Pensions & Auto-Enrolment

A workplace pension is the backbone of most people's retirement — and thanks to auto-enrolment, employer contributions and tax relief, it offers returns available nowhere else. Learn how UK pensions work, why the employer match is 'free money', how tax relief boosts every contribution, and why opting out is usually a costly mistake.

Written by James Lipyeat · Founder, Ironclad Research

Reviewed 17 July 2026 · Editorial policy

Before this, read

Introduction

For most people in the UK, the single most powerful wealth-building tool isn't a clever fund or a hot stock — it's the workplace pension. It's the one place you can get an instant, guaranteed boost on your money from two sources at once: your employer, who adds to it, and the government, which hands back tax on it. Thanks to auto-enrolment, most employees are now signed up by default. Yet many still opt out, or ignore it, leaving enormous value on the table.

This article explains how UK pensions and auto-enrolment work, why the combination of employer contributions and tax relief is so uniquely valuable, and why staying enrolled is one of the easiest good decisions you can make. (For the mechanics of specific account types like SIPPs, see Retirement Accounts; here we focus on the strategy.)

Quick Definition

A pension is a long-term, tax-advantaged savings scheme for retirement. Auto-enrolment is the UK system that automatically enrols eligible employees into a workplace pension — with contributions from you, your employer and tax relief — unless you actively opt out.

Auto-Enrolment: Saving By Default

Left to willpower, most people never get around to starting a pension. Auto-enrolment fixes this by flipping the default: eligible workers are automatically put into their employer's pension scheme, with contributions taken from their pay, unless they take deliberate action to opt out. This simple change — making saving the default rather than a chore — has brought millions into pension saving who otherwise would have had nothing.

The contributions are set at a minimum total percentage of qualifying earnings, split between you, your employer, and tax relief from the government. You can always contribute more than the minimum, and often should, but the automatic minimum is the floor that gets everyone started.

The Contribution Stack: Why £1 Becomes Much More

Here's what makes a pension extraordinary. When you put money in, you're not the only one contributing. Your money is joined by your employer's contribution and by tax relief, so the amount landing in your pot is far more than what left your pay packet.

Two forces drive this:

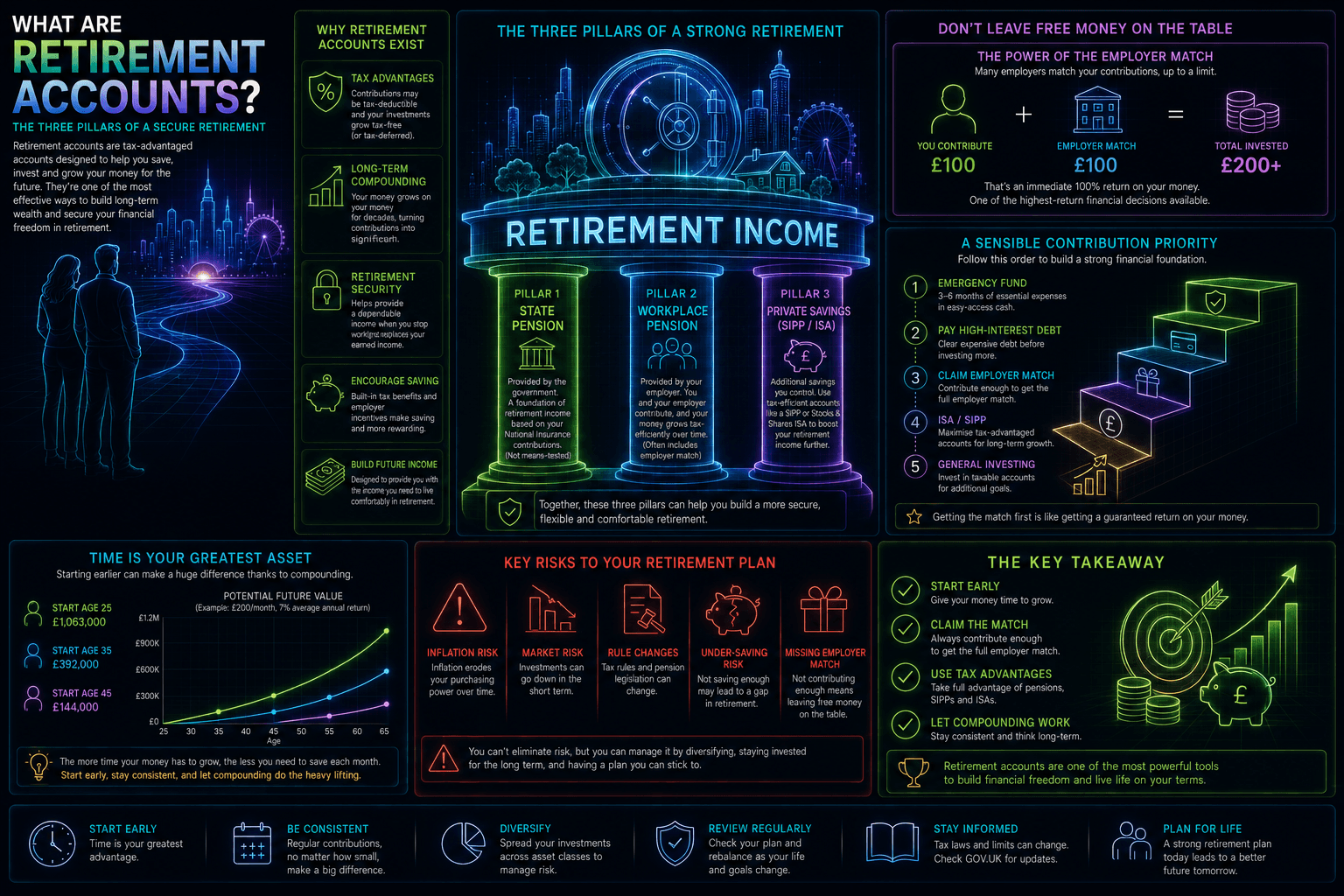

- The employer match — "free money". Your employer contributes on top of yours. This is an immediate, guaranteed uplift — often effectively doubling the minimum contribution — that you get only by staying in the pension. Turning it down by opting out is refusing a pay rise. If your employer matches extra contributions up to a limit, contributing enough to capture the full match is one of the best-value moves in all of personal finance.

- Tax relief. Pension contributions come with tax relief at your income tax rate. For a basic-rate taxpayer, this means £100 in your pension costs only about £80 of take-home pay — the government effectively adds the rest. Higher-rate taxpayers can reclaim even more, making pensions especially powerful for them. (More on this in ISA vs Pension and Tax-Efficient Investing.)

Then, on top of this already-boosted pot, decades of compounding go to work. It's this stack — employer plus tax relief plus compounding — that makes pensions the backbone of retirement.

Defined Contribution vs Defined Benefit

Pensions come in two broad shapes:

- Defined contribution (DC) — the common modern type. You (and your employer) build an investment pot, and its final value depends on how much went in and how the investments performed. The retirement income isn't guaranteed; it depends on the pot you've built.

- Defined benefit (DB) — the older "final salary" type, now rare in the private sector. It promises a guaranteed income in retirement based on your salary and years of service, with the employer bearing the investment risk. If you're lucky enough to have one, it's extremely valuable.

Most people building wealth today are in DC schemes, which is why the size of the pot — driven by contributions, employer match, tax relief and compounding — is what matters.

The State Pension: A Foundation, Not A Plan

The UK also provides a State Pension — a modest, government-paid income in retirement, based on your National Insurance record. It's a valuable foundation, but it's deliberately basic: enough to cover essentials, not enough for the comfortable retirement most people want. Treat it as the floor beneath your own savings, not the whole plan. The gap between the State Pension and the lifestyle you're aiming for is exactly what your workplace and private pensions are there to fill.

Common Misconceptions

"Opting out gives me more money." It gives you slightly more take-home pay now while forfeiting the employer contribution, tax relief, and decades of compounding on all of it. It's one of the most expensive ways to get a small short-term raise.

"The State Pension will be enough." It provides only a basic income. Relying on it alone usually means a significant drop in living standards at retirement.

"Pensions are too complicated to bother with." Auto-enrolment makes the default effortless — you're likely already in one. The powerful part (employer match, tax relief) happens automatically once you simply stay enrolled.

"I'm too young to think about a pension." Youth is your greatest advantage, because of compounding. Contributions in your twenties do far more work than the same contributions later — starting early is the whole game.

Real-World Application

An employee in their first job is auto-enrolled in the workplace pension. Money is coming out of their pay, and it's tempting to opt out to boost their take-home. But consider what opting out really forfeits. Their own contribution is topped up by an employer contribution (free money) and by tax relief (so their bit costs less than it appears), and the whole combined amount then compounds for forty years. By opting out to gain a little cash now, they'd be turning down an immediate, guaranteed uplift on their money and four decades of growth on it — sacrificing a potentially life-changing sum for a marginal short-term gain.

The wiser move is not just to stay enrolled but, if they can, to contribute enough to capture the full employer match, since every matched pound is an instant guaranteed return no investment can promise. They set it up once, let it run automatically, and get on with their life — while their employer and the government quietly help build their retirement in the background. This is wealth building at its most efficient: the tools do the heavy lifting, and the only real decision is not to opt out of them.

Key Takeaways

- A workplace pension is the backbone of UK retirement saving; auto-enrolment signs eligible employees up by default, with an option to opt out.

- What lands in your pot is a stack: your contribution + employer match ("free money") + tax relief — more than you paid before it's even invested.

- Capturing the full employer match is one of the best-value moves in personal finance; opting out forfeits it and the tax relief.

- Most modern schemes are defined contribution (you build a pot); defined benefit (guaranteed income) is now rare but valuable.

- The State Pension is a modest foundation, not a full plan — your own pension fills the gap to a comfortable retirement.

Finished this lesson? Track your progress.

Key terms

Next lesson

Continue learning

ISA vs Pension: Choosing Your Wrapper

Related topics

Retirement Accounts

The big picture of saving for retirement: why tax-advantaged retirement accounts exist, the three pillars (state, workplace and private pensions), why an employer match is free money to claim first, and the priority order for your contributions.

Tax-Efficient Investing

Tax is one of the largest, most avoidable drags on long-term returns — and unlike the market, it's partly within your control. Learn the UK tax allowances that matter, how to shelter investments in ISAs and pensions, the idea of asset location, and simple habits that keep more of your growth compounding for you.

Ironclad Research provides educational content only. Nothing on this platform is financial advice, a recommendation, or an offer to buy or sell any security. Always do your own research and consider professional advice before making financial decisions.