What Is Investing?

A complete, jargon-free introduction to investing: what it really means, why it exists, how returns and compounding work, the main asset classes, and how to think about risk before you begin.

Introduction

Investing is one of the most important financial skills a person can learn — and one of the most widely misunderstood. To some it sounds like the preserve of the wealthy; to others it sounds indistinguishable from gambling. Neither is true.

At its heart, investing is a simple idea: you put money to work today so that it can become more money in the future. This lesson explains exactly what that means, why investing exists at all, how returns are actually generated, and how to think clearly about risk before you ever buy your first asset. No prior knowledge is assumed.

Quick Definition

Investing is committing money today to an asset, while accepting some risk, in the expectation of receiving greater value in the future.

Three words in that sentence carry the weight:

- Asset — something you own that can produce income or grow in value (shares, funds, bonds, property).

- Risk — the possibility that the outcome differs from what you hoped, including the chance of loss.

- Expectation — investing is forward-looking. There are no guarantees, only reasoned expectations based on how assets have behaved over time.

Remove the risk and you no longer have investing — you have saving. Remove the expectation of growth and you are simply spending. Investing lives in the space between the two.

Investing, Saving and Trading

These three words are often used loosely, but they describe genuinely different activities, and confusing them is the source of a great deal of poor decision-making.

- Saving is setting money aside in a form that is stable and accessible — typically a bank or savings account. The nominal balance is protected and you can withdraw at short notice. The trade-off is that returns are low and rarely keep up with inflation, so savings tend to lose real value slowly over long periods.

- Investing is committing money to assets such as shares, bonds or funds for the medium to long term, accepting short-term ups and downs in exchange for higher expected long-term growth. It is patient and ownership-based: you hold productive assets and let time and compounding work.

- Trading is the frequent buying and selling of assets to profit from short-term price movements. It demands far more time, skill and emotional discipline, carries higher costs and taxes, and most people who attempt it underperform a simple long-term investing approach.

This article — and most of what beginners should focus on — is about investing. Saving has its place for short-term needs and emergencies; trading is a specialist pursuit. The instinct to treat investing like trading, by reacting to every market wobble, is one of the most common and costly mistakes new investors make.

Why Investing Exists

To understand why anyone would accept risk with their money, you first have to understand the problem investing solves: cash quietly loses value over time.

Prices across an economy tend to rise year after year — this is inflation. If prices rise by 3% in a year, then £1,000 left untouched buys 3% less than it did twelve months earlier. The number in your account hasn't changed, but its purchasing power has shrunk. Over a single year this is barely noticeable. Over decades it is dramatic.

Investing exists because doing nothing is not actually safe. Leaving money as cash feels safe — the balance never drops — but in real terms it slowly bleeds value. Investing is how people put their money to work so that it can at least keep pace with, and ideally outgrow, inflation.

How Investing Works

When you invest, you exchange money for an asset that you expect to be worth more later, or to pay you along the way, or both. The money doesn't vanish; it changes form. You no longer hold £1,000 in cash — you hold £1,000 worth of a company, a fund, or a loan to a government.

Why would that asset be worth more later? Because it is productive. A share makes you part-owner of a real business that sells goods and services, employs people, and (ideally) earns growing profits. A bond is a loan that pays you interest. A fund bundles many of these together. The value comes from real economic activity, not from someone simply agreeing to pay more later.

Where do returns actually come from?

It is worth pausing on this, because it is the difference between investing and speculation. When you own shares in a business, your return is ultimately driven by that business becoming more valuable — earning higher profits, paying dividends, expanding into new markets. As the economy grows and companies generate more profit over the decades, the businesses you part-own tend to become worth more. You are not hoping that a "greater fool" will pay you more for the same asset; you are sharing in the genuine output of productive enterprises.

This is why broad, long-term investing in the economy has historically rewarded patient investors: it is backed by the collective effort of millions of people working, innovating and producing. It also explains why no single year is predictable — economies expand and contract, sentiment swings — yet the long-run direction has trended upward.

The Two Sources of Return

Every penny of investment return comes from one of two places:

- Income — cash paid to you for holding the asset. Shares may pay dividends (a slice of company profits); bonds pay interest; property pays rent. Income can be spent or, more powerfully, reinvested.

- Capital growth — an increase in the asset's price. If you buy a share for £10 and it later trades at £15, the £5 difference is capital growth (sometimes called a capital gain once you sell).

A single investment can deliver both. Imagine buying shares in a steady, profitable company:

- Year 1: you buy at £10. The company pays a 30p dividend → 3% income.

- Over the year, the share price rises to £10.70 → 7% capital growth.

- Your total return for the year is roughly 10%.

Some investments lean almost entirely on one source. A fast-growing technology company may pay no dividend at all, offering only the prospect of capital growth. A government bond offers steady interest but little growth. Understanding which source you are relying on is central to understanding any investment.

The Engine: Compounding

If there is one idea that makes investing worthwhile, it is compounding — returns that themselves go on to earn returns.

Suppose you invest £1,000 and earn 7% in the first year. You now have £1,070. In the second year, you earn 7% not on your original £1,000 but on the full £1,070 — so you earn £74.90 instead of £70. That extra £4.90 is small, but the effect builds on itself relentlessly. Earlier gains generate their own gains, which generate further gains, and the growth curve steepens over time.

To see the snowball directly, follow a single £1,000 investment growing at 7% a year:

| Year | Value at start | Return earned (7%) | Value at end |

|---|---|---|---|

| 1 | £1,000 | £70 | £1,070 |

| 2 | £1,070 | £75 | £1,145 |

| 5 | £1,311 | £92 | £1,403 |

| 10 | £1,838 | £129 | £1,967 |

| 20 | £3,617 | £253 | £3,870 |

Each year the return earned grows, because it is calculated on an ever-larger balance. By year 20 the annual gain alone (£253) is more than a quarter of the original investment — and you have done nothing but stay invested.

A useful shortcut is the Rule of 72: divide 72 by your annual percentage return to estimate how many years it takes to double your money. At 7% a year, money doubles in roughly 72 ÷ 7 ≈ 10 years. At 9%, about 8 years. The rule is approximate, but it captures something profound — small differences in return, compounded over long periods, produce enormous differences in outcome.

The cost of waiting

This is also why time is an investor's greatest advantage. Consider two people who each invest £200 a month at 7%, but start at different ages and stop at 65:

- Aisha starts at 25 and invests for 40 years. She contributes £96,000 of her own money.

- Ben starts at 35 and invests for 30 years. He contributes £72,000.

Aisha contributes only £24,000 more than Ben — but at retirement she could have roughly £525,000 to Ben's £245,000, more than double. The extra decade at the start, when compounding has the longest runway, does far more work than any amount of catching up later. The single most powerful decision in investing is often simply to begin.

The Main Asset Classes

"Investing" is an umbrella term covering several very different types of asset. Beginners do not need to master all of them, but it helps to know the landscape.

- Shares (stocks) — part-ownership of a company. As a shareholder you participate in the company's profits through dividends and in its growth through a rising share price. Shares have historically delivered the highest long-term returns of the main asset classes, but they also swing the most in the short term: double-digit falls in a single year are entirely normal.

- Bonds — loans to a government or company. In return for lending, you receive regular interest and, eventually, your capital back. Bonds are generally steadier than shares and pay predictable income, which is why they are often used to soften a portfolio's ups and downs — but their expected long-term returns are lower.

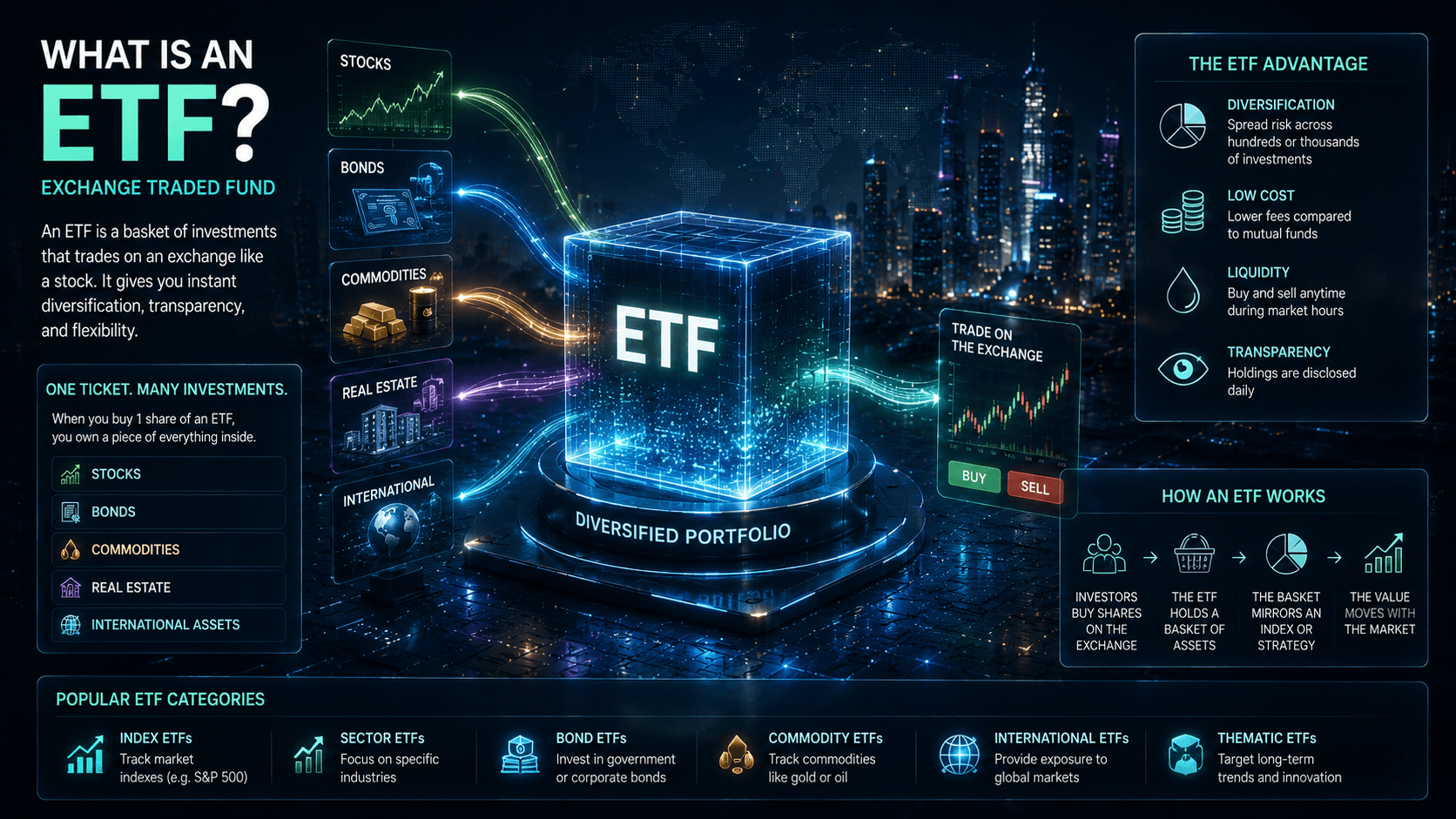

- Funds (including ETFs and index funds) — ready-made baskets that hold many shares or bonds at once. Buying a single broad fund can give you part-ownership of hundreds or thousands of companies in one trade, delivering instant diversification at low cost. For most beginners, a broad, low-cost fund is the natural starting point precisely because it removes the need to pick individual winners.

- Cash and cash-like savings — bank deposits and money-market instruments. The safest in nominal terms (the balance won't fall), but exposed to inflation steadily eroding real value. Ideal for short-term needs and emergency funds, poorly suited to long-term growth.

- Property — physical real estate or property funds. Can provide rental income and capital growth, and many people's largest investment is their home. However, property is illiquid (slow and costly to sell) and often requires large sums or borrowing.

Each sits at a different point on the trade-off between risk and expected return — which is the single most important relationship in all of investing.

Risk and Return

There is no such thing as a free lunch in investing. Assets that offer higher potential returns almost always come with higher risk — a greater chance that the value swings sharply, or that you end up with less than you started. Assets that are very stable tend to offer modest returns.

Crucially, risk is not the same as danger to be avoided at all costs — it is the price of admission for growth. The goal of a thoughtful investor is not to eliminate risk (impossible) but to take an appropriate amount of it, spread it sensibly, and be compensated for it. Two tools do most of the heavy lifting here:

- Diversification — spreading money across many assets so that no single failure is catastrophic. A fund holding 500 companies cannot be wiped out by one of them collapsing.

- Time horizon — the length of time before you need the money. The longer your horizon, the more short-term volatility you can ride out.

The different kinds of risk

"Risk" is not one single thing. A clear-eyed investor recognises several distinct flavours:

- Market risk — the whole market can fall, dragging even good investments down with it. This is the volatility most people picture.

- Inflation risk — the danger that your money grows more slowly than prices rise, quietly reducing what it can buy. This is the risk that cash is most exposed to.

- Concentration risk — the danger of having too much riding on a single company, sector or country. It is the risk that diversification is designed to neutralise.

- Liquidity risk — the difficulty of selling an asset quickly at a fair price when you need to.

A vital distinction sits beneath all of these: the difference between volatility (prices moving up and down) and permanent loss of capital (money you never get back). A diversified portfolio that falls 20% in a downturn has experienced volatility; if you hold on and it recovers, you have lost nothing but composure. Permanent loss is what happens when you are forced to sell at the bottom, or when an undiversified bet on a single company fails completely. Much of sensible investing is about avoiding permanent loss while accepting that volatility is the unavoidable price of growth.

Why Time Horizon Matters

Share prices can fall sharply in any given month or year. But historically, the longer an investor holds a diversified portfolio, the smaller the chance of ending with a loss, because downturns have time to recover and compounding has time to work.

This is why the standard guidance is that money you might need within a year or two generally does not belong in volatile assets — a sudden drop could force you to sell at the worst possible moment. Money you won't touch for ten, twenty or thirty years is exactly the money best suited to investing, because time is on its side.

A Worked Example

Consider a simple, realistic plan: investing £200 per month into a diversified fund, assuming a long-term average return of 7% a year.

- After 10 years, you'd have contributed £24,000. With compounding, the pot might be worth around £34,000.

- After 20 years, contributions total £48,000 — but the pot could be near £100,000.

- After 30 years, contributions total £72,000, while the pot could grow to roughly £240,000.

Notice the pattern: contributions rise in a straight line, but the total accelerates. In the final decade, your money is earning far more from past growth than from new contributions. This is compounding doing the heavy lifting — and it is only available to those who start and stay invested. (These figures are illustrative; real returns vary year to year and are never guaranteed.)

Getting Started: Principles, Not Tips

Beginners often look for a hot tip — the next big stock. But the evidence points somewhere far less glamorous and far more reliable. A handful of durable principles do most of the work:

- Start early and start small. As the cost-of-waiting example showed, time is the most valuable ingredient. A modest amount invested now generally beats a larger amount invested later.

- Invest regularly. Putting money in steadily — say, monthly — removes the impossible task of guessing the perfect entry point and smooths out your average purchase price over time.

- Diversify. Spread risk across many holdings, ideally through broad funds, so no single company or sector can derail you.

- Keep costs low. Fees compound against you just as returns compound for you. Over decades, the difference between a low-cost and a high-cost fund can be enormous.

- Use tax-efficient accounts where available. Many countries offer wrappers — such as ISAs and pensions in the UK — that shelter investments from some tax. The specifics depend on your circumstances, but using them well is often as valuable as choosing the right fund.

- Stay the course. The biggest destroyer of returns is not a market crash; it is selling in a panic during one. A plan you can stick with through downturns beats a perfect plan you abandon.

None of these require predicting the future or beating professionals at their own game. They simply require patience and consistency — which is precisely why investing is accessible to ordinary people, not just experts.

Real-World Applications

Investing is not an end in itself — it is a tool for funding the things people actually care about:

- Retirement — the most common reason to invest. Pensions are, at their core, long-term investment accounts designed to fund the decades after you stop working.

- Major future goals — a house deposit in ten years, a child's education, financial independence.

- Beating inflation — simply preserving the purchasing power of money you've already worked hard to earn.

The right approach depends entirely on the goal and its time horizon. The same person might keep next year's holiday fund in cash, while investing their retirement money in diversified funds for the next thirty years.

Common Misconceptions

- "Investing is just gambling." Gambling has a negative expected return and produces nothing; sound investing means owning productive assets whose value rests on real economic activity, with a positive long-term expectation. The two are not the same.

- "You need a lot of money to start." Many platforms allow investing with very small, regular amounts. Time and consistency matter far more than starting size.

- "I should wait for the perfect moment." Trying to time the market is notoriously difficult even for professionals. For long-term investors, time in the market generally beats timing the market.

- "Higher returns are always better." Higher returns come with higher risk. The best investment is the one whose risk matches your goals and time horizon — not simply the one with the biggest headline number.

Risks & Considerations

Investing carries genuine risk, and honesty about it is essential:

- Capital is at risk. Prices can fall as well as rise, and you may get back less than you put in. There are no guaranteed returns.

- Past performance is not a promise. Long-run historical averages describe the past, not your specific future.

- Inflation and cash both carry risk too. Doing nothing is itself a choice with consequences.

- Risk should be matched to time and temperament. Money needed soon, or that would cause you to panic-sell in a downturn, may not belong in volatile assets.

This article is educational and does not constitute financial advice. Its purpose is to help you understand the mechanics so you can make informed decisions or ask better questions of a qualified professional.

Key Takeaways

- Investing means committing money to a productive asset today, accepting risk, in the expectation of greater value later.

- It exists because idle cash loses real value to inflation over time.

- Returns come from two sources: income (dividends, interest) and capital growth (rising prices).

- Compounding — returns earning returns — is the engine of long-term wealth, and it rewards starting early and staying invested.

- Higher expected returns come with higher risk; diversification and a long time horizon are the main tools for managing it.

- Match your approach to your goal and how long until you need the money.

Finished this lesson? Track your progress.

Next lesson

Continue learning

What Is A Stock?

Related topics

What Is An ETF?

A complete guide to exchange-traded funds: what they are, how they deliver instant diversification, how they track an index, why low costs matter so much, the main types, and the risks.

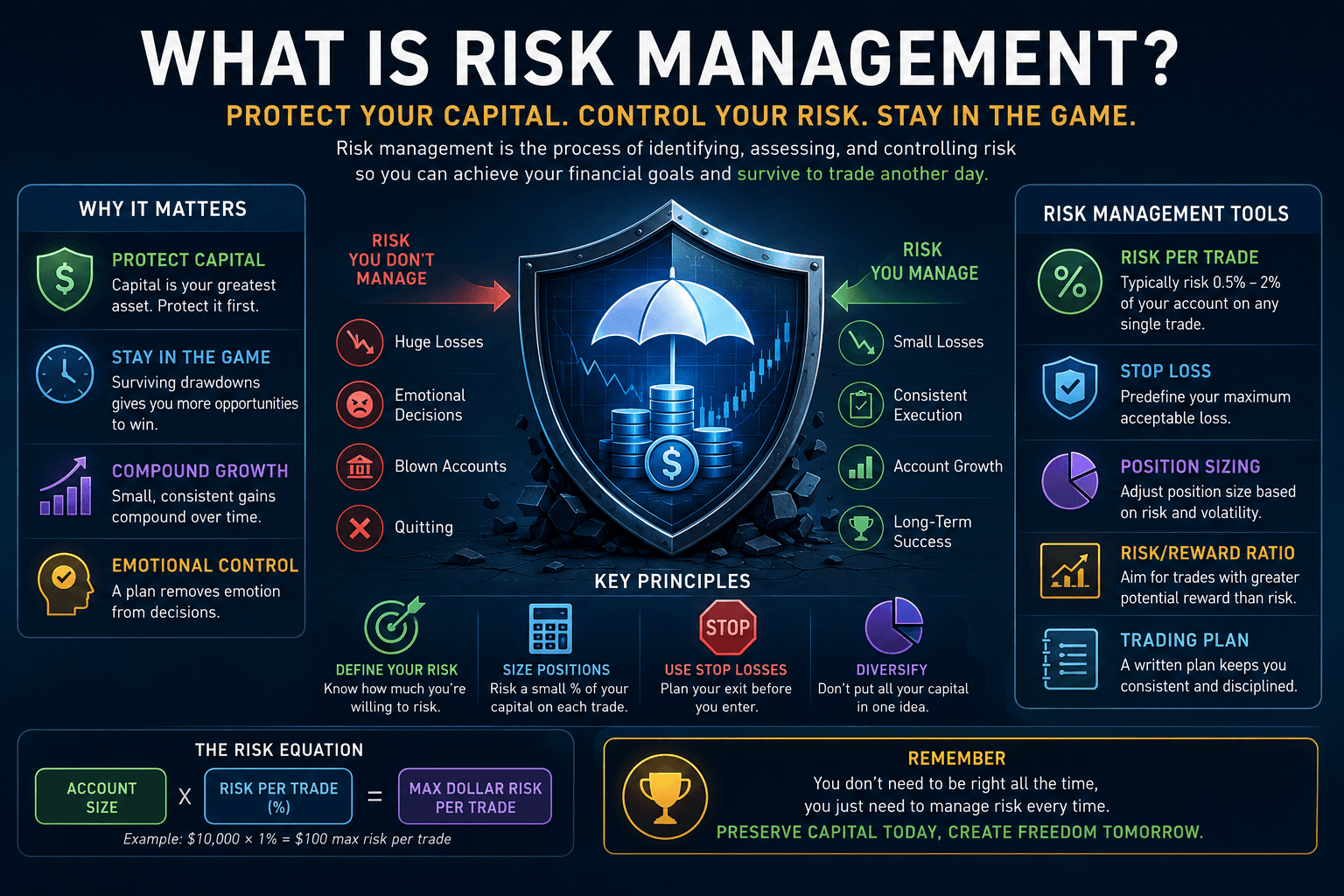

What Is Risk Management?

A practical guide to the discipline that protects investors: why avoiding ruin matters more than maximising gains, the brutal maths of large losses, position sizing, diversification, drawdowns, and matching risk to your goals.

Ironclad Research provides educational content only. Nothing on this platform is financial advice, a recommendation, or an offer to buy or sell any security. Always do your own research and consider professional advice before making financial decisions.