What Is A Stock?

A clear, complete guide to what a share of stock really is — what you own, how shares come to exist, how their price is set, what rights you get, and the risks of owning them.

Before this, read

Introduction

Stocks are the headline of every financial news bulletin. We hear that "stocks rose" or "the market crashed," that someone "made a fortune in shares" or "lost everything." But beneath the drama sits a remarkably simple idea — one that, once understood, demystifies a huge part of the financial world.

This lesson explains exactly what a stock is, what you actually own when you buy one, how shares come into existence, how their price is decided, what rights ownership gives you, and what can go wrong. By the end you will understand not just the definition but the mechanics — the foundation for everything else in investing.

Quick Definition

A stock (or share) is a unit of ownership in a company. Owning one makes you a part-owner of that business, with a claim on a slice of its assets and profits.

Companies divide their ownership into many equal pieces called shares. If a company is carved into one million shares and you own ten thousand of them, you own 1% of the entire business — its factories, its brand, its cash, and its future profits. You are not a customer or a lender; you are an owner, however small.

The words "stock" and "share" are used almost interchangeably. Strictly, "shares" are the individual units and "stock" is the general term for the asset class, but in everyday use the distinction rarely matters.

Why Stocks Exist

To understand shares, it helps to ask why they exist at all. The answer is that companies need money to grow, and selling ownership is one of the two main ways to raise it (the other is borrowing).

Imagine a successful bakery that wants to open fifty new branches. That expansion costs far more than its current profits can fund. The owners have a choice: borrow the money (and owe interest and repayment), or sell a portion of the business to outside investors in exchange for cash. If they sell shares, investors hand over money today and, in return, become part-owners entitled to a slice of all the profits the larger business earns in the future.

This is the genius of the stock market: it lets companies raise large amounts of capital from many investors at once, and it lets ordinary people own a piece of enterprises far bigger than they could ever build alone. The investor's money funds real growth; the company's success flows back to the investor.

The choice between selling shares (equity) and borrowing (debt) shapes the whole nature of a share. A lender must be repaid with interest whether the company thrives or struggles, but has no claim on its success beyond that. A shareholder is the opposite: they are owed nothing and guaranteed nothing, but they own the upside. If the bakery's fifty new branches make it ten times larger, lenders simply get their fixed interest, while shareholders own a stake in a business worth many times more. That asymmetry — limited obligation, unlimited participation — is precisely why shares are riskier than loans and, over the long run, have tended to reward investors more generously for bearing that risk.

What You Actually Own

Owning a share is owning a genuine, if tiny, stake in a real business. Concretely, a share gives you a proportional claim on two things:

- The company's profits — distributed to shareholders as dividends, or reinvested to grow the business (which can raise the share's value).

- The company's net assets — everything it owns minus everything it owes. If the company were sold or wound up, shareholders would have a claim on whatever value remained after debts were settled.

What you do not get is a guarantee. A share is not a loan with a fixed repayment; it is ownership, which means you share in the upside and the downside. If the business thrives, your stake becomes more valuable. If it struggles, your stake can shrink — or, in the worst case, become worthless.

How Shares Come To Exist

A common point of confusion is where shares come from and who gets the money when you buy one. The key is the distinction between two markets.

- The primary market is where a company sells new shares to investors and receives the cash. The most famous example is an Initial Public Offering (IPO), when a private company first lists its shares on a stock exchange and sells them to the public to raise capital.

- The secondary market is where investors buy and sell existing shares from one another. This is what people mean by "the stock market" day to day. When you buy a share of a long-listed company, your money goes to the investor selling it — not to the company itself.

This explains something that puzzles many beginners: a soaring share price does not directly put cash into the company's bank account. It does, however, make it easier and cheaper for the company to raise new capital later, and it reflects investors' collective confidence in the business.

What it means to be "listed"

When a company's shares trade on a public stock exchange — such as the London Stock Exchange, the NYSE or NASDAQ — it is said to be listed or public. Listing brings two big changes. First, the shares become liquid: there is an organised marketplace where buyers and sellers meet continuously, so an owner can usually convert shares to cash quickly at a visible price. Second, the company takes on obligations to disclose — publishing audited accounts and material news on a schedule — so that owners and prospective buyers can judge the business on a level playing field.

The exchange itself does not buy or sell shares; it provides the venue and the rules that let millions of trades happen in an orderly way. Most private companies never list at all — they remain owned by founders, families or private investors — which is why the famous names on the stock market are only a slice of the wider economy. Listing is a deliberate trade: access to large pools of public capital and liquidity, in exchange for transparency and scrutiny.

Common and Preferred Shares

Not all shares are identical. The two broad types are:

- Common (ordinary) shares — the standard kind. They usually carry voting rights and full participation in growth and dividends, but rank last if the company is wound up. This is what most investors hold.

- Preferred shares — these typically pay a fixed dividend and rank ahead of common shares for dividends and in a liquidation, but usually carry no votes and limited upside. They sit somewhere between a share and a bond in character.

For most beginners, "stock" means common shares, and that is the focus here.

How You Make Money From Shares

A shareholder's return comes from the same two sources that drive all investing: income and capital growth.

- Dividends (income). Many established companies distribute part of their profits to shareholders as cash dividends, often quarterly. A company earning steady profits might pay, say, 30p per share per year. Not all companies pay dividends — fast-growing firms often reinvest every penny to grow faster.

- Capital growth. If the share price rises above what you paid, the difference is a capital gain (realised when you sell). Buy at £10, sell at £15, and you have made £5 of capital growth per share.

Consider a simple worked example. You buy 100 shares at £10 each, a £1,000 investment. Over a year:

- The company pays a 30p dividend per share → 100 × £0.30 = £30 of income (a 3% dividend yield).

- The share price rises to £10.80 → £80 of capital growth (8%).

- Your total return is £110, or 11% on your £1,000.

Either source can be zero or negative in a given year — the price can fall, and dividends can be cut. The total return is what matters, and it is never guaranteed.

Dividends, buybacks and reinvestment

A profitable company has three broad choices for the money it earns, and each affects shareholders differently:

- Pay a dividend — return cash directly to shareholders. This is favoured by mature, stable companies whose growth has slowed, and it appeals to investors who want income.

- Reinvest in the business — spend profits on new products, factories or markets. If the reinvestment earns good returns, it can grow future profits and, with them, the share price. Fast-growing companies typically reinvest everything and pay no dividend at all.

- Buy back shares — use profits to repurchase and cancel some of the company's own shares. With fewer shares outstanding, each remaining share represents a larger slice of the business, which can lift its value. Buybacks are, in effect, an indirect way of returning value to shareholders.

This is why shares are often loosely grouped into income shares (established firms paying steady dividends) and growth shares (younger firms reinvesting for expansion, betting on future capital growth). Neither is inherently better; they simply suit different goals and carry different risk profiles.

How The Market Prices A Stock

If the company doesn't set the price on the secondary market, who does? The answer is everyone and no one: the price is simply the level at which buyers and sellers are currently willing to trade. It is set continuously by supply and demand.

What moves that balance? Fundamentally, expectations about the company's future profits. A share is a claim on future earnings, so anything that changes the outlook — strong results, a new product, a recession, a scandal — shifts what investors will pay. This is why prices can jump on news, and even drift on nothing more than a change in mood, while the company's day-to-day operations are unchanged.

A crucial related number is market capitalisation — the total value the market places on the company's equity:

Market cap = share price × number of shares outstanding

This is why share price alone tells you little about a company's size. A £4 share can belong to a company worth far more than a £400 share, depending on how many shares exist. Market cap is the figure investors use to compare companies' sizes.

Valuing the future, not the present

Because a share is a claim on future profits, its price reflects expectations, not just today's results. A widely used sanity-check is the price-to-earnings (P/E) ratio — the share price divided by the company's annual earnings per share. If a company earns £1 per share and trades at £15, its P/E is 15: investors are paying £15 for each £1 of current annual profit.

A high P/E signals that the market expects profits to grow strongly in future; a low P/E suggests modest expectations or perceived risk. This is why two companies with identical profits today can have very different share prices — the market is pricing in different futures. It also explains why a company can report record profits and still see its share price fall: if investors had expected even more, the news disappoints relative to expectations. In the short run, prices track the gap between reality and expectation as much as reality itself.

Over the long run, though, prices are tethered to fundamentals. A business that steadily grows its profits tends to see its share price follow, because sooner or later the earnings justify the valuation. Day to day the market can look like a popularity contest; over years it increasingly resembles a weighing machine.

The Life Of A Share: A Short Story

To tie these threads together, follow a single share through its life.

A profitable software company, owned privately by its founders, decides to expand. To raise £50 million it lists on a stock exchange through an IPO, creating 25 million shares and selling them to investors at £2 each. This is the primary market: the company receives the £50 million and uses it to hire engineers and enter new markets. Its initial market cap is 25 million × £2 = £50 million.

You buy 500 of those shares for £1,000. You are now a part-owner of roughly 0.002% of the company. You did not lend it money; you bought a permanent stake in its future.

Over the next three years the company executes well, and its annual profits double. As results come in, other investors grow more optimistic about its prospects and bid up the price on the secondary market to £3.50. Your 500 shares are now worth £1,750 — £750 of capital growth — even though you have done nothing but hold. Note that this £750 did not come from the company; it reflects what other investors will now pay.

The company, now mature enough to share profits, declares its first dividend of 10p per share. You receive 500 × £0.10 = £50 in income, which you can spend or reinvest into more shares. Meanwhile, management uses some spare cash to buy back shares, slightly shrinking the count and supporting the price.

Then a recession hits. Nervous investors sell, and the price falls to £2.20 — below its recent peak, though still above what you paid. Nothing about the long-term business has fundamentally broken; sentiment has simply soured. An investor with a long horizon holds on; a panicked one sells at the dip and locks in a smaller gain or a loss. This single story contains almost every concept in this lesson: issuance, ownership, the two markets, capital growth, dividends, buybacks, and the gap between price and value.

Shares Within A Portfolio

In practice, few sensible investors put all their money into a single company's shares, however promising. The reason is the residual-claim risk explored above: any one business can fail, and concentrating your wealth in it exposes you to a permanent loss you cannot recover from.

Instead, individual shares are usually held as part of a diversified portfolio — often dozens or hundreds of companies, frequently accessed through funds rather than bought one by one. Diversification means a single company's collapse dents your portfolio rather than destroying it, while you still participate in the long-term growth of businesses as a whole. For many investors, especially beginners, owning the broad market through a fund is the default, with individual shares added selectively for companies they understand and want direct exposure to. Understanding the single share, as in this lesson, is what lets you make those choices deliberately rather than blindly.

Your Rights As A Shareholder

Ownership comes with rights, which vary by company and share class but typically include:

- Voting — common shareholders usually vote on major decisions (electing directors, large mergers), with one vote per share. Your influence is proportional to your stake.

- Dividends — if the company declares a dividend, you are entitled to your share of it.

- Residual claim — a right to your proportional slice of whatever assets remain if the company is wound up, after all other claims are settled.

- Information — listed companies must publish regular financial reports, so owners can see how the business is performing.

Risks & Considerations

Shares offer the highest long-term returns of the major asset classes precisely because they carry real risk. The main ones:

- Price volatility. Share prices move constantly and can fall sharply. A diversified portfolio softens this, but individual shares can be very volatile.

- Business failure. Companies can and do fail. If a company goes bankrupt, its shares can become worthless.

- You are last in the queue. In a wind-up, ordinary shareholders are paid only after employees, tax authorities, lenders and preferred shareholders. The "residual" claim is often residual in the worst sense — nothing left.

- Dilution. If a company issues many new shares, each existing share represents a smaller slice of the business, which can reduce its value.

- No guaranteed income. Dividends are paid at the company's discretion and can be reduced or cancelled at any time.

The standard tools for managing these risks are diversification (owning many companies, often via a fund, so no single failure is catastrophic) and a long time horizon (giving prices time to recover from downturns).

Common Misconceptions

- "A low share price means a cheap, good-value company." Price per share is meaningless without the number of shares. Use market cap, and value the business, not the price tag.

- "Buying shares gives the company my money." Only in the primary market. On the secondary market, your money goes to another investor.

- "Shares always go up over time." Broad, diversified markets have historically trended upward over long periods, but individual shares can fall permanently to zero.

- "Owning shares is the same as running the company." You are an owner, but day-to-day decisions rest with management. Your influence is limited to your votes and your choice to hold or sell.

Real-World Application

Suppose you believe in a company you understand and admire. Buying its shares makes you a part-owner: you participate in its profits through any dividends, benefit if its value grows, and gain a vote in its governance. But a thoughtful investor rarely stakes everything on one company. More commonly, individual shares form part of a diversified portfolio — often alongside funds — so that the success of the whole, rather than the fate of any single business, drives the outcome. Understanding the single share is the foundation; understanding how to combine many is the next step.

Key Takeaways

- A share is a unit of ownership in a company — a claim on its profits and net assets, not a loan.

- Companies issue shares to raise capital; investors buy them to own a slice of the business's future.

- Companies receive money only in the primary market (e.g. an IPO); everyday trading happens between investors in the secondary market.

- Returns come from dividends and capital growth, and neither is guaranteed.

- A share's price is set by supply, demand and expectations; market cap (price × shares) measures the whole company.

- Shareholders rank last if a company fails — the price of their unlimited upside — so diversification and time are essential.

Finished this lesson? Track your progress.

Key terms

Next lesson

Continue learning

What Is A Broker?

Related topics

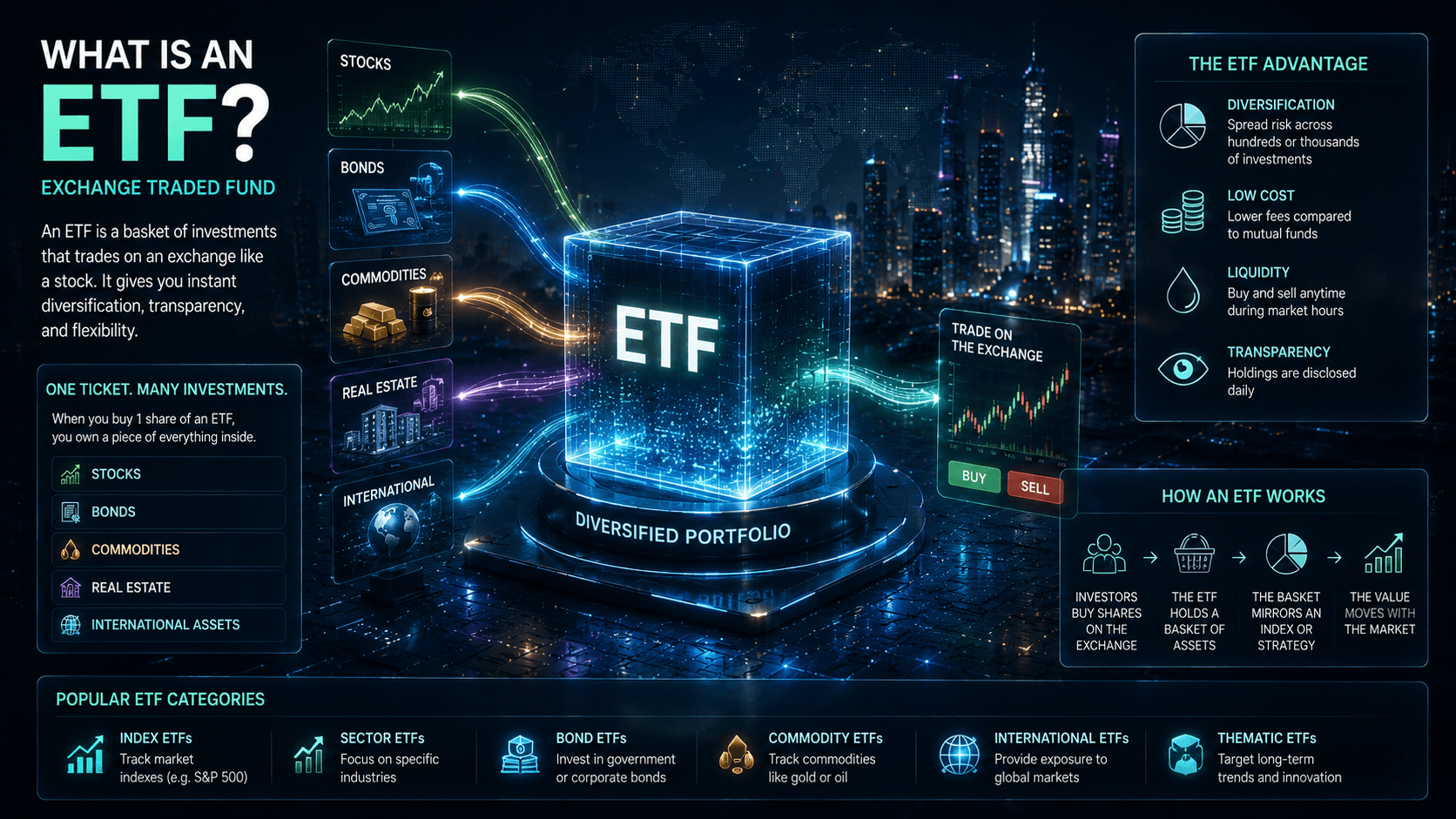

What Is An ETF?

A complete guide to exchange-traded funds: what they are, how they deliver instant diversification, how they track an index, why low costs matter so much, the main types, and the risks.

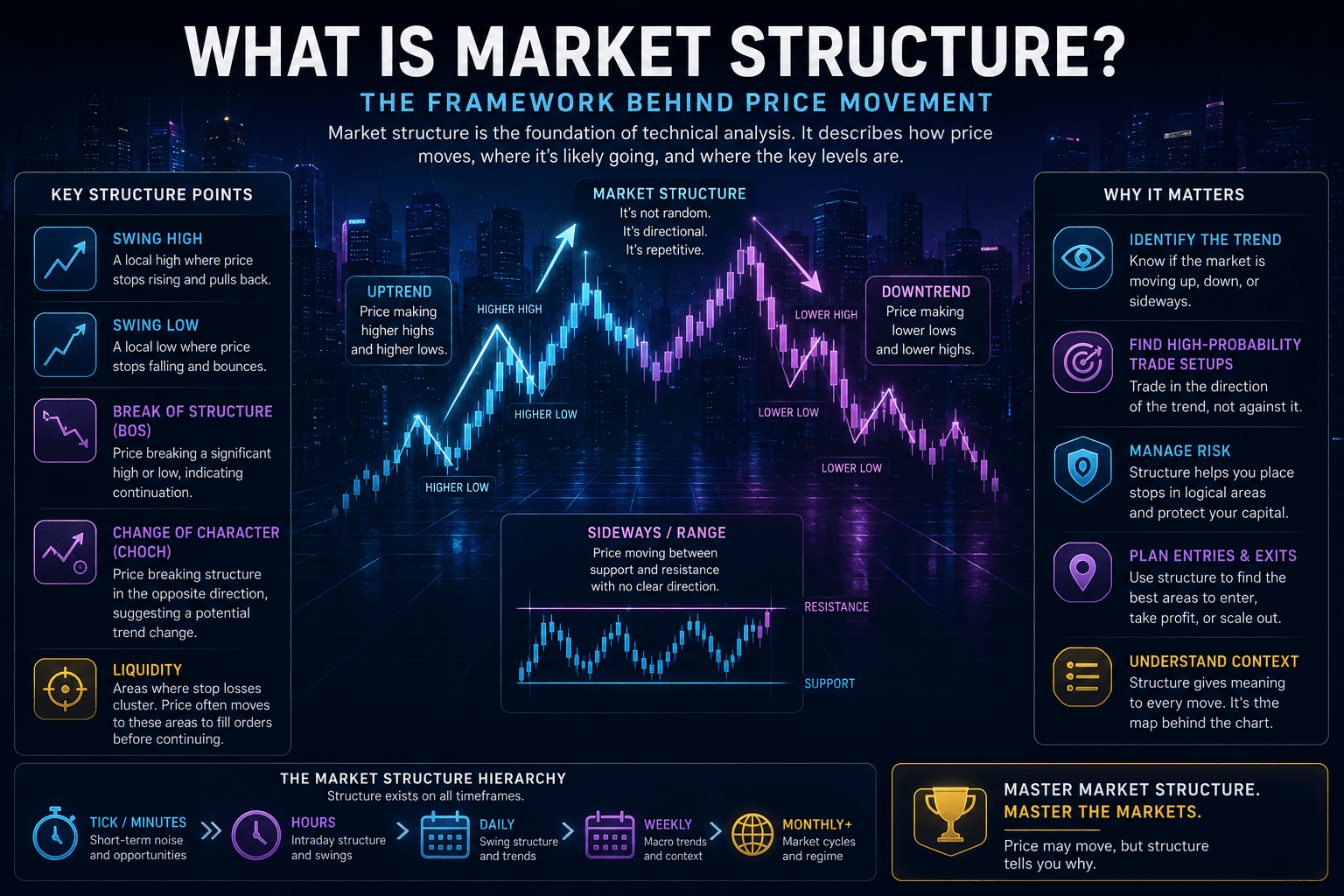

What Is Market Structure?

A guide to the hidden plumbing of the markets: the players, how a trade really travels from your tap to settlement, what the order book and liquidity mean, lit venues versus dark pools, and why it all affects the price you get.

Ironclad Research provides educational content only. Nothing on this platform is financial advice, a recommendation, or an offer to buy or sell any security. Always do your own research and consider professional advice before making financial decisions.