What Is A Broker?

A complete guide to brokers: what they do, why you need one, how they actually make money, the journey of an order, how your shares are held, and how to choose one safely.

Before this, read

Introduction

You have decided to invest. You know what a share is and why owning productive assets can build wealth over time. But how do you actually buy one? You cannot walk up to a stock exchange and ask for ten shares. Between you and the market stands an essential intermediary: the broker.

Brokers are so woven into modern investing that most people use one without thinking about what it really does or how it earns its keep. This lesson pulls back the curtain: what a broker is, why the market is built so that you need one, what happens in the seconds after you tap "buy," how your shares are actually held, how brokers make money — including the parts they would rather you not notice — and how to choose one you can trust.

Quick Definition

A broker is a regulated firm that gives investors access to financial markets, routing and executing their orders and holding their accounts.

In plain terms, a broker is the bridge between you and the market. You tell it what you want to buy or sell; it carries out the transaction on your behalf, holds the resulting assets and cash in your account, and handles the administrative machinery of settlement, record-keeping and reporting. It is, in effect, your authorised agent in a marketplace you cannot enter alone.

Why Brokers Exist

To see why brokers are necessary, you have to understand how exchanges work. A stock exchange does not transact with the general public. It deals only with its member firms — a closed set of professional institutions that meet its capital, technology and regulatory requirements. An individual cannot simply connect to the exchange's order book.

The broker solves this. As a regulated member (or by connecting through one), it has the legal standing, the technology and the relationships to place your order into the market. It also handles the unglamorous but vital work of holding your assets securely, settling trades, collecting your dividends, producing tax documents and keeping accurate records. Without brokers, markets would be accessible only to large institutions, and ordinary people would be locked out.

What A Broker Actually Does

Behind the simple "buy" button, a broker performs several distinct functions:

- Order taking — providing the app, website or phone line through which you instruct it.

- Routing and execution — deciding where to send your order and getting it filled at the best available terms.

- Custody — safekeeping your shares and cash, usually in a ring-fenced client account.

- Settlement — completing the exchange of cash for shares after a trade, typically one business day later (known as T+1).

- Administration — collecting dividends, handling corporate actions (such as stock splits), and producing statements and tax reporting.

A good broker makes all of this invisible. But understanding that it is happening helps you judge what you are paying for and where things can go wrong. It is worth dwelling on one of these functions in particular, because it is so easy to take for granted: custody. When you own shares through a broker, you are trusting it to keep accurate records of what you own and to safeguard those assets indefinitely — through market crashes, corporate takeovers, dividend payments and your own years of inactivity. The quality of that record-keeping, and the legal protections around it, matter just as much as the price you pay to trade. A broker is not merely a button that buys shares; it is the long-term custodian of your financial life, which is why the questions of regulation and asset protection discussed later in this lesson are not technicalities but the heart of the decision.

From Trading Floors To Apps

It helps to see how dramatically the role of the broker has changed, because it explains why investing is so accessible today. For most of the twentieth century, buying shares meant telephoning a stockbroker — often a person you knew — who would charge a hefty commission, perhaps tens or even hundreds of pounds, to relay your order to a colleague standing on a noisy exchange floor. Share certificates were physical pieces of paper, posted to you and stored carefully at home or in a vault. Investing was slow, expensive and largely the preserve of the wealthy.

Three changes transformed this. Electronic markets replaced the trading floor, so orders could be matched by computers in milliseconds. The internet let investors place those orders themselves, removing the need for a human middleman on every trade. And dematerialisation turned paper certificates into electronic book entries, making custody cheap and instant. The combined effect was to collapse the cost of trading from hundreds of pounds to pennies — or, with payment for order flow, to an apparent zero. The modern trading app in your pocket is the end point of that century-long journey: the same essential function — connecting you to the market — delivered faster and cheaper than the wealthiest investor of the past could have dreamed. Understanding this history also makes the modern trade-offs clearer: when something becomes "free," the cost has usually been relocated, not removed.

Types Of Broker

Not all brokers are the same. Broadly, they fall into a few categories:

- Full-service brokers offer advice, research, financial planning and a personal relationship — at a higher cost. They suit investors who want guidance and are willing to pay for it.

- Execution-only (discount) brokers simply carry out the orders you decide on, with no advice. Most modern online platforms and trading apps are execution-only, and their low costs have made investing far more accessible.

- Robo-advisors sit in between, using software to build and manage a diversified portfolio for you based on your goals and risk tolerance, usually for a modest annual fee.

For most self-directed investors today, a low-cost execution-only platform is the norm. The trade-off is clear: you save on fees but take full responsibility for your own decisions.

Cash Accounts And Margin Accounts

Whichever broker you choose, you will open one of two fundamental account types, and the distinction matters enormously for risk.

A cash account is the simple, sensible default. You can only buy investments with money you have actually deposited. If you have £1,000 in the account, you can buy up to £1,000 of shares. Your losses are limited to the money you put in, and there is no borrowing involved. For the overwhelming majority of investors — and certainly all beginners — a cash account is the right choice.

A margin account lets you borrow money from the broker to buy more than your cash allows, using your existing investments as collateral. With £1,000 of cash you might control £2,000 of shares, borrowing the other £1,000. This magnifies outcomes in both directions: a 10% rise turns a larger profit, but a 10% fall turns a larger loss. Worse, if your investments fall far enough, the broker can issue a margin call, demanding you add cash immediately — and if you cannot, it can sell your holdings, potentially at the worst possible moment, to repay the loan. Margin also accrues interest, one of the broker's revenue streams noted above.

Margin is a genuine tool for experienced investors who understand leverage, but it converts the ordinary risk of investing into something that can wipe out an account quickly. The single most protective decision a new investor can make is to stick to a cash account until they thoroughly understand what borrowing to invest really entails.

How Brokers Make Money

This is the part many investors never examine, yet it shapes everything from the price you get to the conflicts a broker may face. Even a broker advertising "zero commission" is a business that must generate revenue. The main streams are:

- Commissions — a straightforward fee charged per trade. Once standard, these have fallen sharply or vanished at many retail brokers.

- The spread — some brokers quote a slightly worse price than the true market price, pocketing the difference. This is a hidden cost baked into the price you receive.

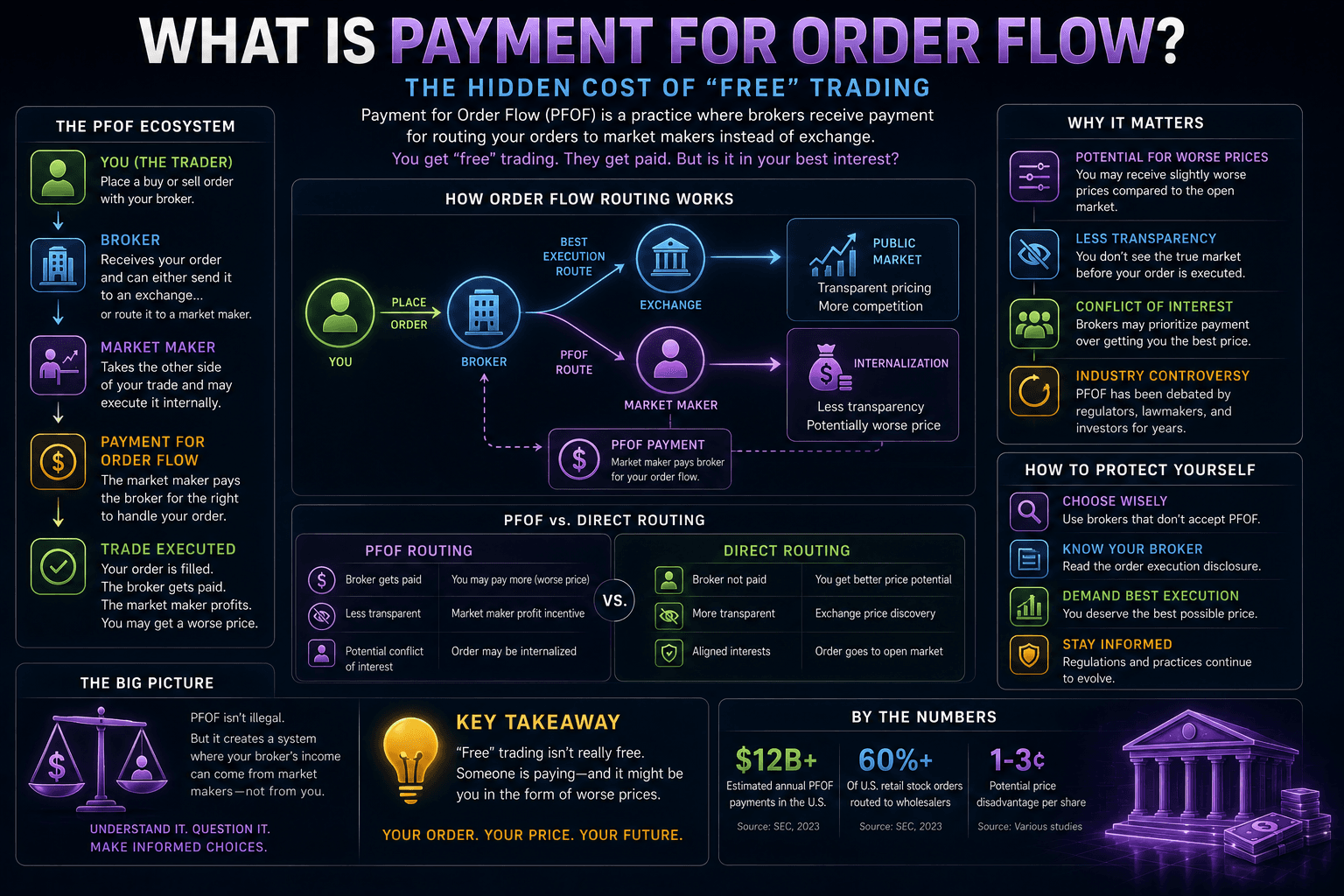

- Payment for order flow (PFOF) — instead of charging you, the broker sells the right to execute your orders to large trading firms (market makers), which pay for the steady stream of retail orders. This funds much "free" trading, but it raises questions about whether your order is routed for your benefit or the broker's.

- Margin interest — brokers lend investors money to buy more than their cash allows, and charge interest on those loans.

- Interest on uninvested cash — your idle cash earns the broker interest, only some of which (if any) is passed to you.

- Securities lending — brokers can lend out the shares held in client accounts to other market participants (for example, short sellers) and earn a fee.

- Account and currency fees — platform fees, withdrawal charges and, especially, currency-conversion fees on foreign shares.

The key insight: "free" rarely means free. When commissions disappear, the cost usually moves to a less visible place. Understanding which streams a broker relies on tells you where its incentives lie — a theme explored in depth in the companion lesson on payment for order flow.

The Journey Of An Order

When you tap "buy," a surprising amount happens in under a second:

Your broker decides where to send the order — to an exchange, an alternative venue, or a market maker. How well it does this (the price and speed you get) is called execution quality, and it is one of the most important and least visible differences between brokers. Once matched with a counterparty, the trade is filled, and a day or so later it settles: cash and ownership officially change hands. The choices a broker makes at the routing step are exactly where payment for order flow can create a tension between your interests and the broker's.

Telling your broker how to trade: order types

You also control how the order is executed, through the order type you choose. The two you will use most are:

- A market order says "buy (or sell) now, at the best available price." It prioritises certainty of execution over price: it will almost always fill immediately, but in a fast-moving or thinly traded market the price you get can differ from the one you saw — a phenomenon called slippage.

- A limit order says "buy (or sell) only at this price or better." It prioritises price over certainty: you will never pay more than your limit, but the order may not fill at all if the market never reaches your price.

For a heavily traded share, a market order is usually fine because the spread is tiny and there are many buyers and sellers. For a thinly traded one, a limit order protects you from a poor fill. Most brokers also offer stop orders, which become active only once a price level is breached and are often used to limit losses, though they carry their own pitfalls in volatile conditions. Understanding order types means the difference between trading on your own terms and leaving the outcome to chance — and it costs nothing but a moment's thought before you confirm.

How Your Shares Are Held

A subtle but important point: when you buy shares through most brokers, your name does not appear on the company's official share register. Instead, the broker holds your shares in a nominee account — a pooled account in the broker's name (or its custodian's), with the broker's internal records showing that you are the beneficial owner.

This arrangement makes trading fast and cheap, and regulated brokers must keep client assets ring-fenced from their own, so they are protected if the broker fails. But it also means you rely on layers of intermediaries and the records they keep — a topic explored further in the lessons on market structure and direct registration (DRS), which describes the alternative of registering shares directly in your own name.

What happens if a broker fails?

This is the question that worries new investors most, and the answer is reassuring but worth understanding precisely. Because a regulated broker must hold your assets separately from its own, your shares and cash are not part of the broker's own balance sheet. If the firm goes bankrupt, its creditors generally cannot claim your ring-fenced assets; they should be identifiable as yours and either transferred to another broker or returned to you.

The complication is that administration is slow and records are not always perfect. If client assets turn out to be missing — through fraud or sloppy record-keeping, for example — that is where an investor-protection scheme steps in. In the UK the Financial Services Compensation Scheme (FSCS) can compensate clients of a failed authorised firm up to a per-person limit; in the US the equivalent is SIPC. These schemes are a backstop for the failure of the firm, not insurance against your investments falling in value — a crucial distinction. A share that drops 40% in a market downturn is an ordinary investment risk that no scheme covers. Protection schemes exist solely to address the loss of assets caused by a broker's collapse, and only up to their stated limits, which is one more reason to favour well-capitalised, properly regulated brokers and, for large sums, to consider spreading assets across more than one.

Why Regulation Comes First

Before any comparison of fees or features, one question outranks all others: is the broker properly regulated? A regulated broker operates under the supervision of a financial authority — the Financial Conduct Authority (FCA) in the UK, the SEC and FINRA in the US, and equivalents elsewhere. That supervision is not a rubber stamp; it imposes concrete protections that directly affect the safety of your money.

Regulated firms must, among other things, keep client assets segregated from their own, maintain minimum levels of capital so they can absorb shocks, follow rules on treating customers fairly and executing their orders well, and submit to audits and reporting. They are also typically members of an investor-protection scheme that backstops client losses if the firm fails. An unregulated "broker" — particularly the slick, unsolicited platforms that proliferate online — offers none of this. If it disappears with your money, you may have no recourse at all.

Checking regulation takes minutes and is the single highest-value piece of due diligence an investor can perform. Reputable regulators publish public registers of authorised firms; you can confirm that a broker is listed, that its name and details match exactly, and that it is permitted to offer the services you want. Be alert to clone scams, where fraudsters copy a real firm's name and credentials. A genuine investment that loses value is an acceptable, understood risk; handing your money to an unregulated or fraudulent platform is not investing at all. No advertised feature, bonus or zero-commission promise is worth bypassing this check.

What To Look For In A Broker

With regulation confirmed, the remaining factors help you choose between legitimate options:

- Regulation — is the broker authorised by a credible regulator? This is non-negotiable.

- Investor protection — is it covered by a compensation scheme (such as the FSCS in the UK or SIPC in the US) that protects client assets up to a limit if the firm fails?

- Costs — not just headline commissions, but spreads, platform fees, currency-conversion charges and withdrawal fees. The cheapest-looking broker is not always the cheapest overall.

- Execution quality — how good are the prices you actually receive?

- Range of assets and accounts — does it offer the investments and tax-efficient account types (such as ISAs or pensions) you need?

- Reliability and support — does the platform stay up during volatile markets, and can you reach a human when something goes wrong?

Risks & Considerations

- Broker failure. A broker can go bust. Regulated client-money rules and protection schemes are designed to return your assets or compensate you up to a limit, but this is why choosing a properly regulated firm matters so much.

- Hidden costs. "Free" trading shifts costs to spreads, currency fees and order-flow arrangements. Always look for the total cost of ownership, not the advertised price.

- Conflicts of interest. When a broker is paid to route your orders a certain way, its incentives may not perfectly align with getting you the best price.

- Margin. Borrowing from your broker magnifies both gains and losses and can force the sale of your holdings at the worst time. It is an advanced tool, not a beginner's convenience.

Common Misconceptions

- "My broker owns my money, so I could lose it if they fail." Regulated brokers must ring-fence client assets separately from their own, and protection schemes add a further backstop — though limits apply.

- "Commission-free means it costs nothing." The cost has simply moved somewhere less visible.

- "The broker decides which investments are good." An execution-only broker gives you access and tools; the decisions — and the responsibility — are yours.

- "All brokers give the same price." Execution quality varies, and over many trades the difference adds up.

Real-World Application

Imagine opening your first investment account. You compare two platforms: one charges a small commission per trade but is transparent and gives excellent prices; the other is "commission-free" but earns through payment for order flow and a currency markup on foreign shares. For a long-term investor making occasional purchases, the headline-free platform might actually cost more once spreads and FX fees are included. Knowing how brokers make money lets you see past the marketing, weigh the total cost, confirm the firm is regulated and protected, and choose the one whose incentives best align with yours. The broker is the foundation of your investing life — choosing well, once, pays off for years.

Key Takeaways

- A broker is the regulated intermediary that gives you access to markets and executes and holds your investments.

- You need one because exchanges deal only with member firms, not the public.

- Brokers make money in many ways — commissions, spreads, payment for order flow, margin interest, interest on cash, securities lending and fees — so "free" is rarely free.

- When you trade, the broker routes your order to a venue; the quality of that routing affects the price you get.

- Most shares are held in a nominee (street-name) account: you are the beneficial owner, but not the registered holder.

- Choose a broker on regulation, investor protection, total cost and execution quality — not the headline price alone.

Finished this lesson? Track your progress.

Key terms

Next lesson

Continue learning

What Is An ETF?

Related topics

What Is Payment For Order Flow?

A balanced explanation of payment for order flow: how it funds commission-free trading, why market makers pay for retail orders, the conflict of interest it creates, price improvement and the NBBO, and what it means for you.

What Is A Stock?

A clear, complete guide to what a share of stock really is — what you own, how shares come to exist, how their price is set, what rights you get, and the risks of owning them.

Ironclad Research provides educational content only. Nothing on this platform is financial advice, a recommendation, or an offer to buy or sell any security. Always do your own research and consider professional advice before making financial decisions.