ISA vs Pension: Choosing Your Wrapper

ISAs and pensions are the two great UK tax wrappers — and choosing between them (or using both well) shapes how much of your wealth you keep. Learn how each treats money going in, growing and coming out, the trade-off between tax relief and access, and a sensible priority order for your contributions.

Written by James Lipyeat · Founder, Ironclad Research

Reviewed 17 July 2026 · Editorial policy

Before this, read

Introduction

The UK gives investors two superb tax shelters: the ISA and the pension. Used well, they mean the taxman takes far less of your wealth over a lifetime; used poorly, or not at all, you hand over money you never needed to. The trouble is they work in almost opposite ways — one rewards you on the way in, the other on the way out — and choosing between them (or, better, combining them) is one of the most consequential decisions in wealth building.

This article compares the two wrappers head to head: how each treats your money going in, while it grows, and coming out; the central trade-off between tax relief and access; and a sensible order for deciding where your next pound should go. (For the account mechanics themselves, see ISAs, SIPPs and Retirement Accounts.)

Quick Definition

An ISA is a tax wrapper funded with already-taxed money, growing tax-free and withdrawn tax-free, with full access anytime. A pension is funded with tax relief (and often an employer match), grows tax-free, but is taxed as income on withdrawal and locked until a minimum pension age.

Three Stages, Two Opposite Designs

Every tax wrapper can be judged at three points: money going in, money growing, and money coming out. Here's how the two compare.

- Going in: the pension wins. Contributions get tax relief at your income tax rate, and workplace pensions add an employer match — free money the ISA simply can't offer.

- Growing: a tie. Both shelter all growth, income and gains from tax while invested.

- Coming out: the ISA wins. ISA withdrawals are entirely tax-free; pension withdrawals are taxed as income (beyond a tax-free lump sum), because the break was given on the way in.

- Access: the ISA wins decisively. ISA money is available anytime; pension money is locked until a minimum pension age.

The Central Trade-Off: Relief vs Access

Strip it down and the choice is this: the pension offers more tax advantage (relief plus match), but at the cost of locking your money away until pension age. The ISA offers less tax advantage but complete flexibility. You're essentially paying for the pension's generosity with access.

This makes the "better" wrapper depend on your situation:

- A pension is especially powerful if you get an employer match (always grab that first), you're a higher-rate taxpayer (relief at 40%+ is very valuable), and you won't need the money before pension age. The most attractive case: getting relief at the higher rate going in, then paying only basic rate on withdrawal in retirement — a genuine tax win.

- An ISA is better if you might need access before pension age, you want flexible tax-free income, or you're saving for a goal that comes before retirement (a house deposit, a career break). Its flexibility is worth forgoing some tax relief for.

A Sensible Priority Order

For most people, a reasonable order for each spare pound looks like this:

- Capture the full employer pension match — it's an instant, guaranteed return nothing else matches. Never leave it on the table.

- Clear expensive debt (not covered here, but it usually beats investing).

- Then choose based on access and tax: higher-rate taxpayers and long-locked retirement money often favour further pension contributions; those wanting flexibility or nearer-term access favour the ISA.

- Use both over time. Many people build a pension for the tax-efficient core of retirement and an ISA for flexible, accessible wealth — the pension for the long lock-up, the ISA for everything in between.

This isn't one-size-fits-all, and tax rules change, but the logic — match first, then weigh relief against access — is durable.

Common Misconceptions

"ISAs are always better because withdrawals are tax-free." The pension's tax relief and employer match on the way in often outweigh the ISA's tax-free exit — especially for higher-rate taxpayers. It's a genuine trade-off, not a clear win either way.

"Pensions are worse because they're taxed on withdrawal." They're taxed on the way out instead of the way in — and the relief plus match going in, compounding for decades, frequently makes them the more valuable wrapper despite the exit tax.

"I should only use one." Most people benefit from both: the pension for its unmatched tax relief on locked-away retirement money, the ISA for flexible, accessible savings. They complement rather than compete.

"The employer match is optional." It's the closest thing to free money in finance. Capturing the full match should come before almost any other investing decision.

Real-World Application

A higher-rate taxpayer is deciding where to put £1,000 of savings. In a pension, higher-rate relief means that £1,000 effectively costs them far less of their take-home pay, an employer match may add still more, and it all compounds for decades. When they eventually draw it in retirement — likely as a basic-rate taxpayer — they get a tax-free lump-sum portion and pay only basic-rate tax on the rest. Getting relief at 40%+ and paying tax at perhaps 20% is a favourable swing that the ISA can't replicate. For long-term retirement money they won't touch until pension age, the pension is the clear winner here.

But the same person is also saving for a possible career break in eight years — well before pension age. For that money, locking it in a pension would be a mistake; they can't access it when they need it. So they use an ISA, accepting no tax relief in exchange for the ability to withdraw, tax-free, whenever the break comes. Same investor, same tax rate — but the purpose and timing of the money sent each pound to a different wrapper. That's the real skill: not declaring one wrapper "best", but matching each to the job it's doing. Used together, the pension and ISA cover the whole span of a financial life.

Key Takeaways

- Pensions give tax relief (plus an employer match) going in but tax withdrawals and lock money until pension age; ISAs give no relief in but are tax-free and accessible anytime. Both grow tax-free.

- The core trade-off is tax relief vs access — the pension's generosity is paid for with a lock-up.

- Pensions shine for the employer match, for higher-rate taxpayers, and for money you won't need until retirement; ISAs shine for flexibility and pre-retirement goals.

- A sensible order: grab the full employer match first, then weigh relief against access for the rest.

- Most people are best served using both, matching each pound to its purpose and timing.

Finished this lesson? Track your progress.

Key terms

Next lesson

Continue learning

Tax-Efficient Investing

Related topics

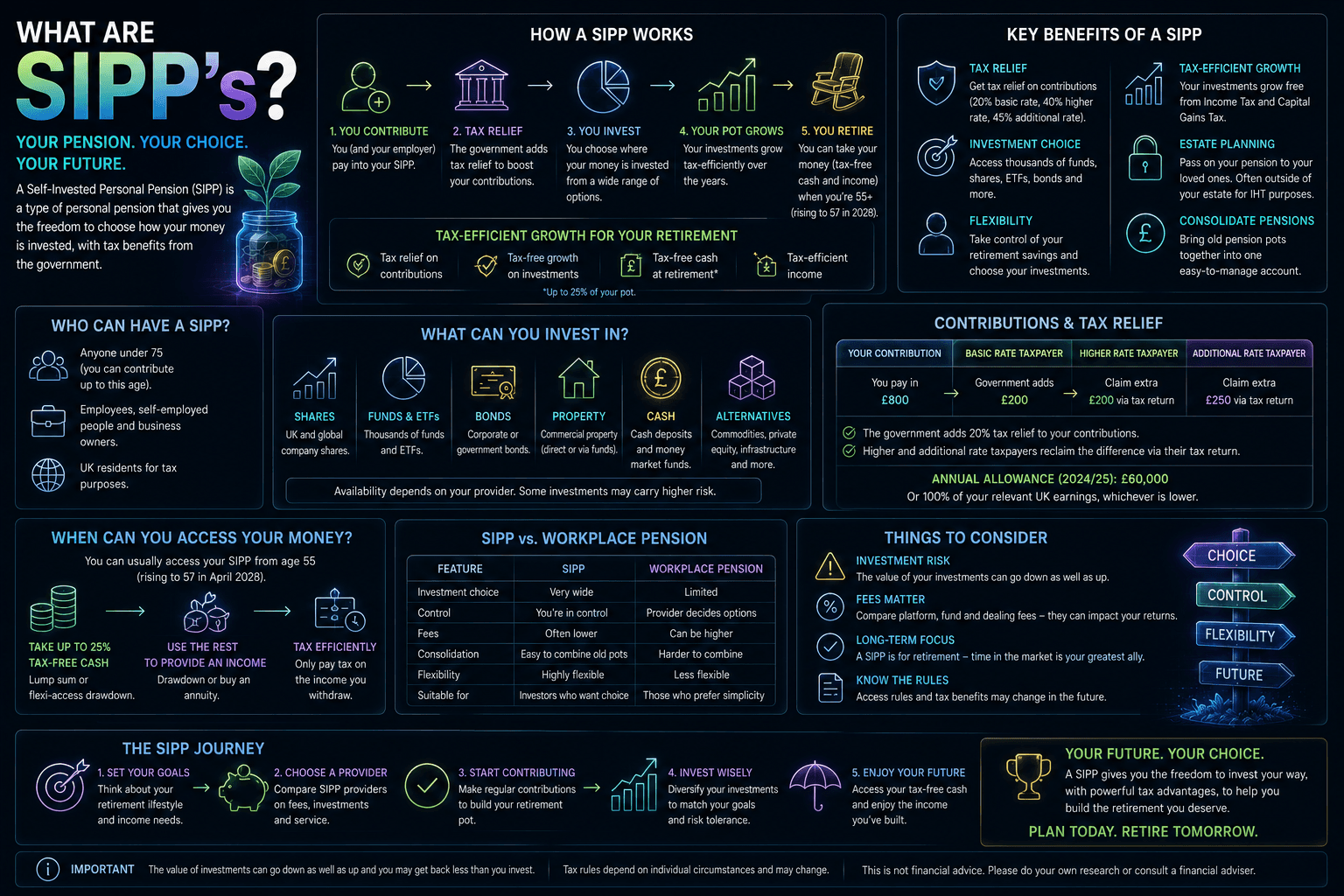

SIPPs

The UK's self-invested personal pension: how a SIPP works, the tax relief that boosts contributions, why the money is locked until a minimum age, how withdrawals are taxed, and how it compares with an ISA.

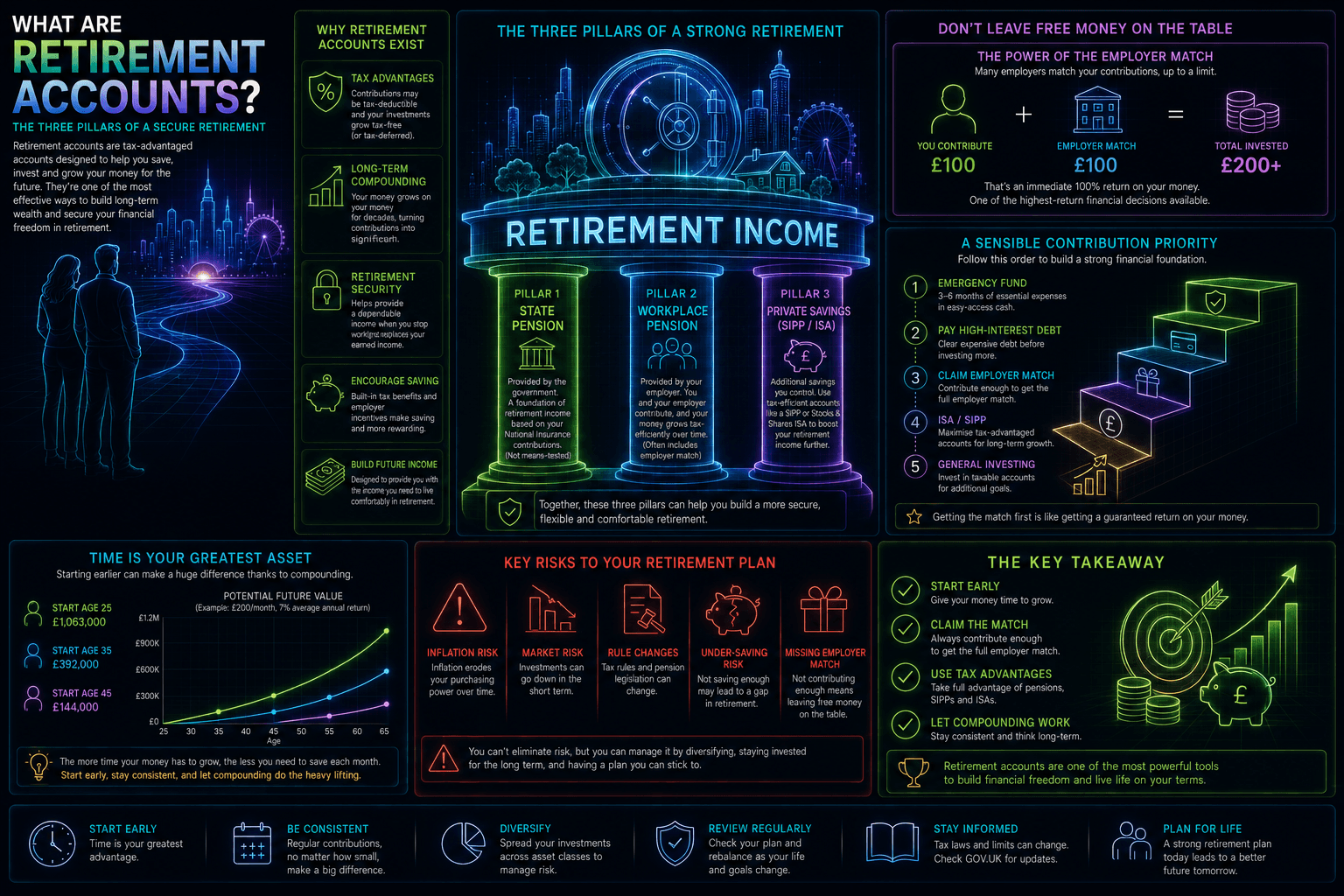

Retirement Accounts

The big picture of saving for retirement: why tax-advantaged retirement accounts exist, the three pillars (state, workplace and private pensions), why an employer match is free money to claim first, and the priority order for your contributions.

Ironclad Research provides educational content only. Nothing on this platform is financial advice, a recommendation, or an offer to buy or sell any security. Always do your own research and consider professional advice before making financial decisions.