ISAs

The UK's tax-free wrapper for saving and investing: what an ISA is, the main types, the annual allowance, why tax-free growth and withdrawals matter so much over time, and how the Stocks & Shares ISA fits a long-term plan.

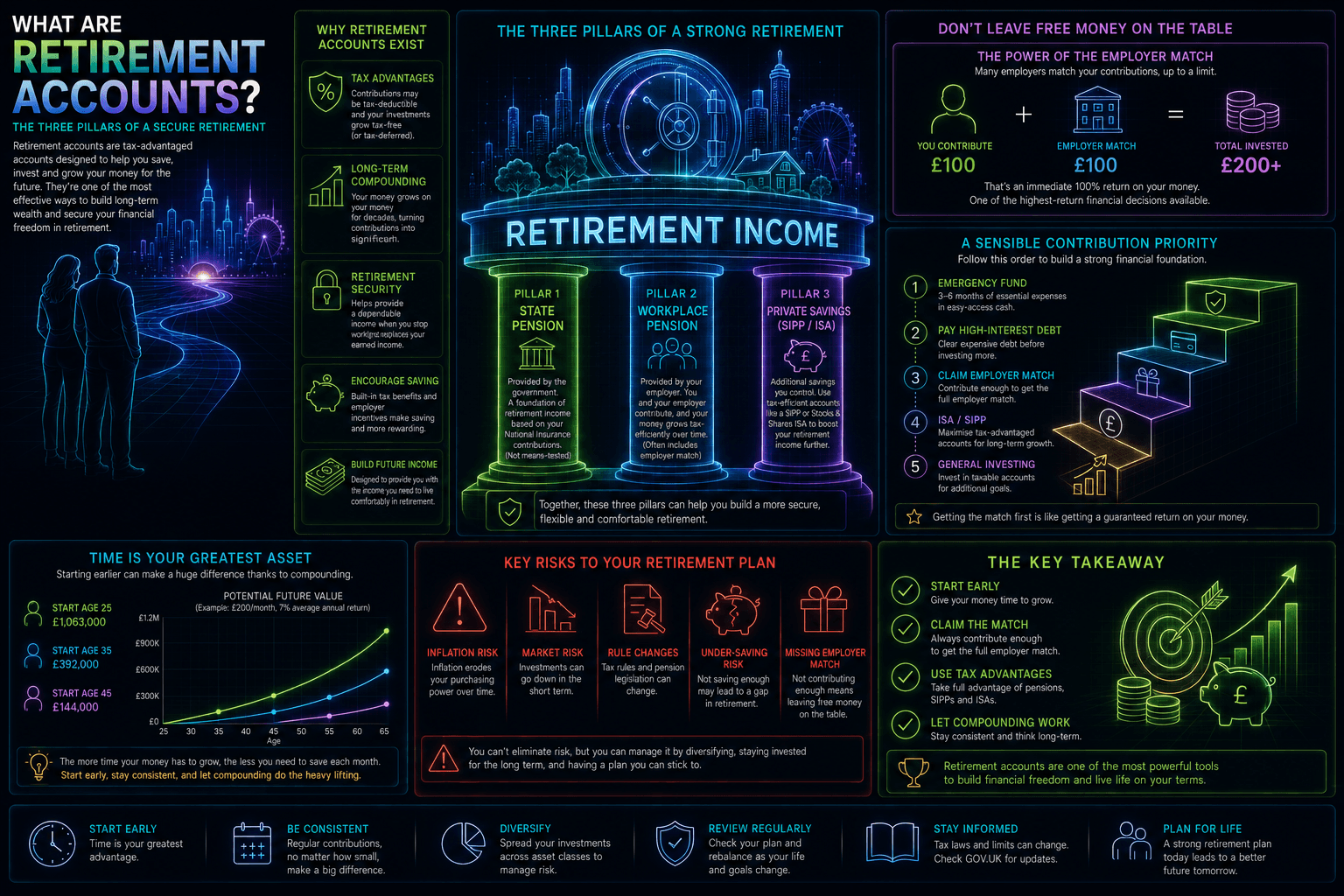

Before this, read

Introduction

In the UK, one of the most valuable tools available to an ordinary investor isn't an investment at all — it's a wrapper that goes around your investments and shelters them from tax. It's called an ISA, and using one well can make a substantial difference to how much of your returns you actually keep over a lifetime. For many UK investors, "should I use an ISA?" is one of the highest-impact financial questions there is — and the answer, for most, is yes.

This lesson explains what an ISA is, the main types, the annual allowance, and — most importantly — why tax-free growth and withdrawals matter so much when compounded over decades. It focuses on the Stocks & Shares ISA most relevant to investing, and shows how it fits alongside pensions like the SIPP. (Tax rules are UK-specific and can change; this is education, not tax advice.)

Quick Definition

An ISA (Individual Savings Account) is a UK tax-free "wrapper": money held inside it grows free of income tax and capital gains tax, and you can withdraw it tax-free, at any time.

The crucial idea is that an ISA is not itself an investment — it's a tax-protected container you put investments (or cash) into. The same fund held in an ISA versus a normal taxable account behaves identically in the market, but inside the ISA, the taxman doesn't take a slice of your gains, your dividends, or your withdrawals. Over time, that sheltering is worth a great deal.

How An ISA Works

You open an ISA with a provider (a bank, building society or investment broker), pay money in up to the annual limit, and choose what to hold inside it. From then on, everything that happens inside the wrapper is shielded from UK tax: no capital gains tax when your investments rise and you sell, no income tax on dividends or interest, and no tax on withdrawals whenever you take money out.

This is different from a normal ("general investment") account, where gains above an annual exemption can be subject to capital gains tax and dividends above an allowance can be taxed. By holding the same investments inside an ISA, you remove that tax drag entirely. There's no tax to declare, no gains to calculate — the ISA does the sheltering automatically.

The Main Types Of ISA

"ISA" is an umbrella term; several types exist, each suited to a different purpose:

- Cash ISA — holds cash savings, with tax-free interest. Suited to short-term, safety-first money — though, like all cash, exposed to inflation over the long run (see Inflation).

- Stocks & Shares ISA — holds investments (funds, shares, bonds). This is the one most relevant to long-term investing, sheltering growth and income from tax. The focus of this lesson.

- Lifetime ISA (LISA) — designed for a first home or later-life saving, with a government bonus but specific rules and restrictions.

- Innovative Finance ISA — holds peer-to-peer lending and similar; more niche and higher-risk.

You can split your annual allowance across different ISA types in a tax year, within the overall limit. For most people building long-term wealth, the Stocks & Shares ISA is the workhorse.

The Annual Allowance

ISAs come with an annual allowance — a cap on how much you can pay in across your ISAs each tax year. The allowance resets each tax year, and crucially, unused allowance generally can't be carried forward: if you don't use this year's space, it's gone for good.

The practical implication is that, where you can afford to, filling (or at least using) your ISA allowance each year captures valuable tax-free space that disappears if unused. You don't have to use it all — invest only what suits your circumstances — but understanding the use-it-or-lose-it nature helps you prioritise the ISA when deciding where to put your investing money. (The exact allowance figure is set by the government and can change, so check the current limit.)

Why Tax-Free Growth Matters So Much

The real power of an ISA reveals itself over decades, through compounding. In a taxable account, tax can nibble at your returns along the way — on dividends, and on gains when you sell — and each pound lost to tax is a pound that no longer compounds. Inside an ISA, the full return compounds, year after year, untouched.

The effect is the same compounding magic described in Compound Growth, but applied to tax. Sheltering even a modest amount of annual tax drag, compounded over twenty or thirty years, can leave you with a noticeably larger final pot than the identical investments held in a taxable account.

And there's a second, subtler benefit: simplicity. Because ISA gains and income are tax-free, there's nothing to report, calculate or declare — no capital-gains paperwork, no dividend tax to track. For long-term investors, the ISA offers both a financial edge and a quiet life. Over a lifetime of investing, that combination is hard to beat.

Getting Started With An ISA In Practice

Putting this to use is straightforward. You open a Stocks & Shares ISA with an investment broker (comparing them on cost and features, as in Choosing A Broker), pay in what you can afford up to the annual allowance, and invest it — for many beginners, into a broad, low-cost fund (see What Is An ETF?). From there, the wrapper does its work automatically: everything inside grows and can be withdrawn tax-free.

A few practical habits help. Automate contributions where possible (paying yourself first, as in Financial Goals), so the allowance is used steadily rather than scrambled for at year end. Hold long-term, growth-oriented investments in the Stocks & Shares ISA, since that's where tax-free compounding has the most to shelter. And remember the wrapper is just the container — the investing principles from the rest of the curriculum (diversification, low costs, patience) still apply inside it. An ISA used well is not complicated; it's simply the default home for most UK investors' long-term, accessible money.

ISA vs Pension: Different Jobs

An ISA is not the only tax-advantaged wrapper — pensions like the SIPP (covered in SIPPs) are the other major one — and they do different jobs. The key contrast is access versus tax relief:

- An ISA offers tax-free growth and withdrawals, with flexible access — you can take money out anytime, tax-free. Great for goals before retirement, or for flexibility.

- A pension offers tax relief on contributions (a boost going in) but locks the money until a minimum age, with tax usually due on withdrawal. Great specifically for retirement.

Neither is universally "better" — they suit different goals, and many people use both. The broad principle (explored further in Retirement Accounts) is to match the wrapper to the job: an ISA for flexible, accessible long-term investing, a pension for money specifically earmarked for retirement, where the contribution boost is most valuable.

Risks & Considerations

- An ISA shelters tax, not market risk. Investments inside a Stocks & Shares ISA still rise and fall — the wrapper protects from tax, not from losses.

- Rules can change. Allowances, types and rules are set by the government and can be altered; check current rules rather than relying on old figures.

- Cash ISAs face inflation risk. Tax-free interest is still interest — over the long term, cash can lose real value (see Inflation).

- Allowance is per person, per year. Use-it-or-lose-it means planning helps, but never contribute more than your circumstances allow.

Common Misconceptions

- "An ISA is an investment." It's a tax wrapper around investments (or cash), not an investment itself.

- "ISAs are only for cash savings." The Stocks & Shares ISA holds investments and is central to long-term investing.

- "Money in an ISA is locked away." Unlike a pension, ISA money is generally accessible anytime, tax-free.

- "An ISA protects me from losing money." It protects from tax, not from market falls — the investments inside can still drop.

Real-World Application

Consider two UK investors who each invest £5,000 a year into the same diversified fund for thirty years — one inside a Stocks & Shares ISA, one in a taxable general account. They earn identical market returns. But along the way, the taxable investor loses a slice of their dividends to income tax and pays capital gains tax when rebalancing or selling, while the ISA investor pays nothing and reports nothing. After three decades, the ISA investor ends up with a meaningfully larger pot — and a far simpler tax life — purely from sheltering the same returns from tax. They didn't pick better investments or take more risk; they simply used the wrapper. For most UK investors, that is the everyday, compounding value of the ISA.

Key Takeaways

- An ISA is a UK tax-free wrapper: investments inside grow free of income and capital gains tax, with tax-free withdrawals.

- The Stocks & Shares ISA is the key type for investing; others include Cash, Lifetime and Innovative Finance ISAs.

- The annual allowance is use-it-or-lose-it — using it where you can captures tax-free space permanently lost otherwise.

- Tax-free growth compounds powerfully over decades and brings welcome simplicity (no gains to report).

- An ISA (flexible access) and a pension (contribution tax relief, locked) do different jobs — match the wrapper to the goal.

- An ISA shelters tax, not market risk — investments inside still rise and fall.

Finished this lesson? Track your progress.

Key terms

Next lesson

Continue learning

SIPPs

Related topics

Ironclad Research provides educational content only. Nothing on this platform is financial advice, a recommendation, or an offer to buy or sell any security. Always do your own research and consider professional advice before making financial decisions.