Compound Growth

The most powerful force in investing: how returns earning returns turns modest sums into large ones over time, the three levers that drive it, why starting early matters most, and how compounding can work against you too.

Before this, read

Introduction

Albert Einstein is often quoted — probably apocryphally — as calling compound interest the eighth wonder of the world. Whether or not he said it, the sentiment is right: compound growth is the single most powerful force in investing, the quiet engine that turns modest, regular savings into substantial wealth over a lifetime. It is also routinely underestimated, because human intuition is built for straight lines, while compounding curves upward in a way that feels almost magical once it gets going.

This lesson explains exactly how compounding works, the difference between simple and compound growth, the three levers that drive it, and — crucially — why time is the most important of them. We will work through real numbers, meet the handy Rule of 72, and confront the sobering flip side: compounding works against you too, through fees, inflation and debt. It builds on What Is Investing? (where compounding first appeared) and pairs naturally with Inflation and Building Wealth.

Quick Definition

Compound growth is the process by which your returns themselves earn returns, so that growth builds on previous growth and accelerates over time.

The contrast that makes it click is with simple growth. With simple growth, you earn a return only on your original sum. With compound growth, last year's gains are added to your balance, and this year you earn a return on that larger balance too. Each period's growth becomes part of the base for the next period's growth — an ever-expanding snowball. Over short periods the difference is small; over long periods it becomes enormous.

Simple vs Compound: The Snowball Begins

Picture £1,000 earning 10% a year. With simple interest, you'd earn a flat £100 every year — £100 in year one, £100 in year ten, forever linear. With compound interest, you earn 10% of the current balance each year: £100 in year one (on £1,000), but £110 in year two (on £1,100), £121 in year three (on £1,210), and so on, growing every year.

This divergence is the whole story of compounding. In the early years the two lines are almost indistinguishable, which is why compounding feels slow and unrewarding at first and why so many people give up before it pays off. But the curve is patient and relentless: given enough time, the compound line pulls away so far that the simple line looks flat by comparison. The lesson is to start, and then to wait.

A Worked Example, Year By Year

Numbers make it concrete. Here is £10,000 growing at 8% a year, with nothing added:

| Year | Balance at start | Growth (8%) | Balance at end |

|---|---|---|---|

| 1 | £10,000 | £800 | £10,800 |

| 2 | £10,800 | £864 | £11,664 |

| 5 | £13,605 | £1,088 | £14,693 |

| 10 | £19,990 | £1,599 | £21,589 |

| 20 | £43,157 | £3,453 | £46,610 |

| 30 | £93,173 | £7,454 | £100,627 |

Look at the "growth" column: in year one it's £800; by year 30 it's £7,454 — nearly the entire original investment earned in a single year, without you adding a penny. The £10,000 has become over £100,000, a tenfold increase, purely through compounding. And notice where most of that happened: the balance roughly doubled from year 20 to year 30 alone. Compounding back-loads its rewards into the later years, which is the single most important practical fact about it.

The Three Levers Of Compounding

Three factors determine how much your money compounds. Understanding them tells you exactly where to focus.

- Rate of return — the annual percentage your money earns. Higher rates compound faster, but chasing high returns means taking on more risk (see Risk vs Reward), so this lever has limits and dangers.

- Time — how long the money compounds. Because growth accelerates, time has an outsized, non-linear effect — and it's the lever most within your control if you simply start early.

- Contributions — how much you add along the way. Regular contributions feed the snowball, and combined with time and compounding they do remarkable work.

Of these, time is the quiet giant, because it multiplies the effect of the other two. A modest rate over a long period routinely beats a high rate over a short one, and contributions made early compound for far longer than the same contributions made late.

Why Starting Early Wins

The dominance of time produces one of the most important — and counter-intuitive — lessons in personal finance: starting early can beat investing more money later.

Take two people who each invest £200 a month at 7%, stopping at 65. Aisha starts at 25 and invests for 40 years, contributing £96,000 of her own money. Ben starts at 35 and invests for 30 years, contributing £72,000. Aisha contributes only £24,000 more than Ben — but at retirement she could have roughly £525,000 to Ben's £245,000, more than double. That extra decade at the start, when compounding has the longest runway, does vastly more work than any amount of catching up later. The reason ties back to the year-by-year table: the latest years of compounding are the most powerful, and only the early starter gets to keep them. The single most valuable decision in investing is often simply to begin.

How Often Does It Compound?

A natural question is how frequently compounding happens — yearly, monthly, daily? The more often returns are added to the balance and start earning their own returns, the faster the snowball rolls, though the effect of frequency is smaller than people expect. The leap from simple interest to annual compounding is large; the further leaps from annual to monthly to daily add progressively less.

In practice, you rarely need to manage this directly. Savings accounts state how often interest is added; investment returns compound continuously as prices rise and as reinvested income buys more assets. What matters far more than frequency is the three big levers — rate, time and contributions — and the discipline of reinvesting rather than withdrawing. Don't agonise over compounding frequency; focus on staying invested for a long time at a reasonable cost, and the frequency takes care of itself.

The Rule Of 72

You don't need a calculator to estimate compounding's pace. The Rule of 72 is a handy shortcut: divide 72 by your annual percentage return to estimate how many years it takes to double your money.

| Annual return | Years to double (72 ÷ rate) |

|---|---|

| 3% | ~24 years |

| 6% | ~12 years |

| 8% | ~9 years |

| 10% | ~7 years |

| 12% | ~6 years |

The rule is approximate, but it captures something profound: small differences in return produce large differences in outcome over time. The gap between 6% and 8% looks minor, but it's the difference between doubling your money every 12 years versus every 9 — over a long life, several extra doublings. This is also why fees matter so much (a 2% fee can cost you a whole doubling), and why the patient pursuit of a reasonable return for decades beats gambling on a spectacular one.

Compounding Cuts Both Ways

Compounding is not always your friend. The same exponential mathematics that builds wealth can destroy it, working silently against you in three ways:

- Fees. Investment costs compound against you exactly as returns compound for you. A seemingly small 1% annual fee, over decades, can quietly consume a large fraction of your final wealth — every pound paid in fees is a pound that never compounds. This is why low-cost investing matters so much.

To put a number on it: £100,000 growing at 7% for 30 years becomes about £738,000 at a 0.1% fee, but only about £574,000 at a 1.0% fee — a difference of roughly £164,000, lost entirely to a fee gap that sounded trivial. That is compounding working against you, and it's why a fraction of a percent in costs is one of the most consequential numbers in your financial life.

- Inflation. As covered in Inflation, rising prices compound too, steadily eroding the purchasing power of money — which is why beating inflation is the minimum bar, and why cash loses ground over time.

- Debt. Compounding interest on borrowing is compounding in reverse and against you. High-interest debt, like credit cards, can snowball as viciously as investments grow — which is why clearing expensive debt is often the highest-return "investment" available.

The symmetry is worth internalising: compounding is a force, not a friend. Pointed at productive assets over a long horizon, it builds fortunes; pointed at fees, inflation or debt, it erodes them. The investor's job is to put as much of it as possible on their own side.

What Return Should You Realistically Expect?

The examples here use rates like 7–8% because those roughly reflect the long-run historical average of diversified stock-market investing, before inflation. But it's important to set honest expectations around three caveats.

First, these are long-run averages, not annual guarantees. Real markets are lumpy — a year might be +25% or −20%; the average only emerges over many years, and there are long stretches of disappointment along the way. Compounding rewards those who stay invested through the bad years to capture the good ones. Second, the figures are usually quoted before inflation; the real (after-inflation) return is several percentage points lower, which matters for any long-term plan. Third, past performance is not a promise — history is the best guide we have, not a contract for the future.

The practical implication is to plan with reasonable, even slightly conservative, assumptions rather than optimistic ones, and to treat any single year's result as noise around a long-term trend. Compounding is powerful precisely because it works over decades; judging it over months or a single year misses the point entirely and tempts the very impatience that destroys it. Set realistic expectations, and the maths will look after the rest.

The Role Of Reinvestment

One practical mechanism powers much of compounding's magic: reinvestment. When an investment pays income — dividends from shares, interest from bonds — you can either take that cash out or plough it back in. Reinvesting means that income buys more of the asset, which then generates its own income, which is reinvested in turn. This is compounding made tangible, and over decades the difference between spending income and reinvesting it is staggering. Many funds (the "accumulating" type mentioned in What Is An ETF?) do this automatically. For anyone in the wealth-building phase, reinvesting income rather than spending it is one of the simplest, most powerful ways to let compounding work at full strength.

Common Misconceptions

- "Compounding isn't worth it unless I have a lot to invest." The mechanism works on any amount; time and consistency matter more than starting size, and small sums become large given enough years.

- "I'll start later when I earn more." Delay is compounding's greatest enemy — the early years you skip are the most valuable, as the cost-of-waiting example shows.

- "A high return is all that matters." Time and low costs often matter more; a reasonable return compounded for decades beats a high one over a short period or one eaten by fees.

- "Compounding only helps me." Fees, inflation and debt compound against you with the same power — direct the force deliberately.

Real-World Application

Imagine a 25-year-old who can spare just £150 a month. It feels too small to matter, and the temptation is to wait until they earn more. But invested steadily at a long-term average return of around 7%, that modest habit could grow to well over £350,000 by retirement — the overwhelming majority of it being growth, not contributions, generated by compounding over four decades. The same person starting at 40 instead would end with a small fraction of that, despite contributing for many of the same years. Nothing about this requires picking winning stocks or timing the market; it requires only starting early, keeping costs low, reinvesting, and letting time do the heavy lifting. That is compound growth in real life: not a trick, but patience, mathematically rewarded.

Key Takeaways

- Compound growth is returns earning returns — growth building on growth, accelerating over time into an upward curve.

- It differs from simple growth (linear) and back-loads its biggest gains into the later years, so it rewards patience.

- Three levers drive it — rate, time and contributions — and time is the most powerful, which is why starting early can beat investing more money later.

- The Rule of 72 (72 ÷ return = years to double) shows how small differences in rate or fees compound into large differences over time.

- Compounding works against you too — through fees, inflation and debt — so keep costs low, beat inflation, and clear expensive debt.

- Reinvesting income lets compounding work at full strength; the key action is simply to start, and stay invested.

Finished this lesson? Track your progress.

Next lesson

Continue learning

Financial Goals

Related topics

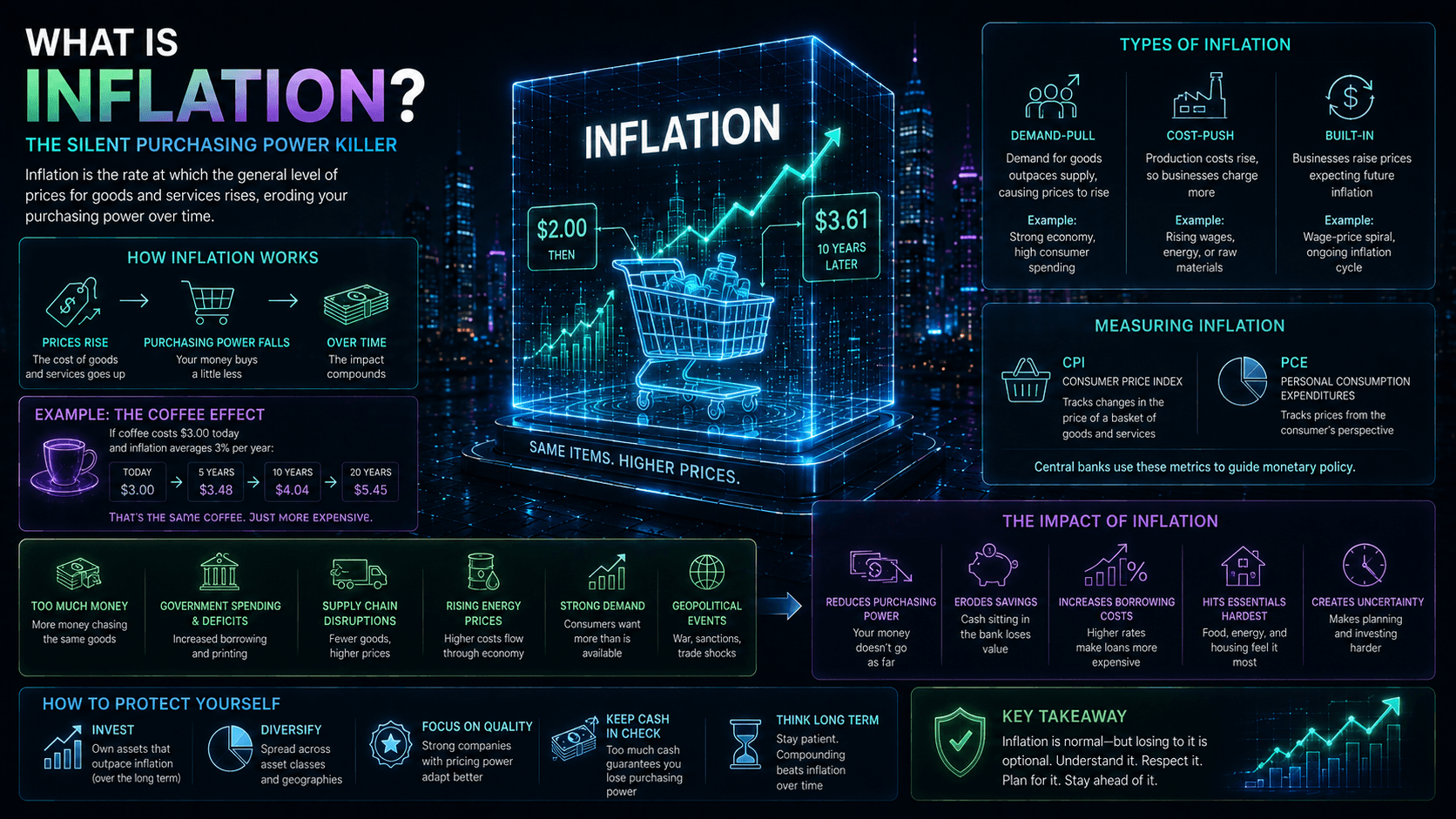

Inflation

Why the slow rise in prices is the quiet force every investor must beat: what inflation is, how it's measured, the difference between real and nominal returns, how it erodes idle cash, and how different assets hold up against it.

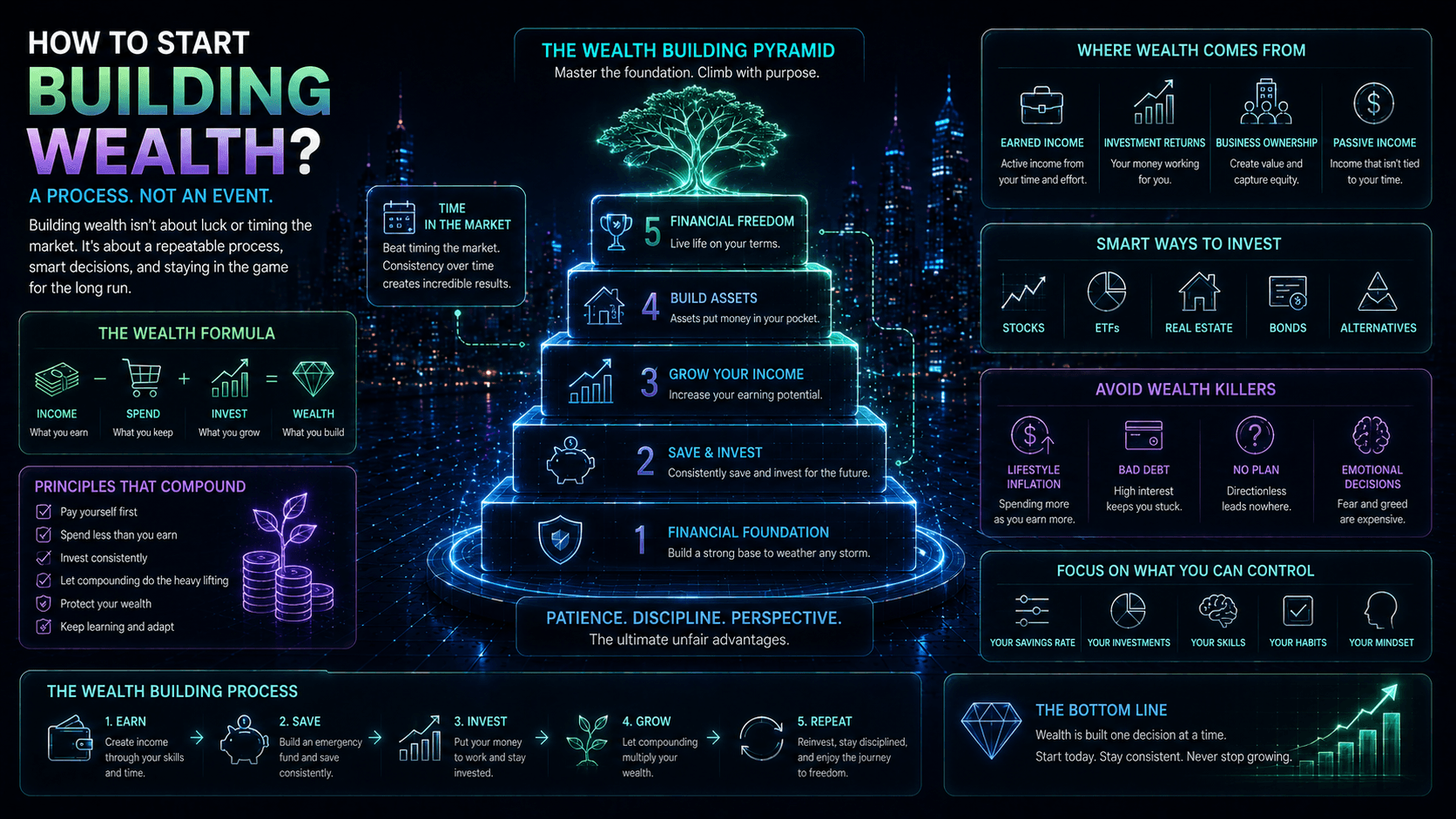

Building Wealth

How wealth is actually built: the simple equation of earning more than you spend and investing the gap, why your savings rate matters more than your income, the power of consistency, and how to protect what you grow.

Ironclad Research provides educational content only. Nothing on this platform is financial advice, a recommendation, or an offer to buy or sell any security. Always do your own research and consider professional advice before making financial decisions.