Building Wealth

How wealth is actually built: the simple equation of earning more than you spend and investing the gap, why your savings rate matters more than your income, the power of consistency, and how to protect what you grow.

Before this, read

Introduction

This lesson ties together everything in the Getting Started curriculum. You've learned what investing is, how it differs from trading, the trade-off between risk and reward, how inflation erodes idle money, how compounding multiplies invested money, and how to set financial goals. Building wealth is what happens when you put all of it into practice, consistently, over time.

The good news — and it genuinely is good news — is that building wealth is far simpler than most people imagine. It does not require a high income, special access, or the ability to pick winning stocks. It requires a basic equation, applied with patience and discipline over years. This lesson lays out that equation, explains why your savings rate often matters more than your income, why consistency beats brilliance, and how to protect what you build so a single setback doesn't undo years of progress.

Quick Definition

Building wealth is the long-term process of spending less than you earn, investing the difference, and allowing it to compound — repeated consistently over time.

That's the whole secret, and it fits in a sentence. There is no hidden trick that the wealthy know and you don't. Wealth is the accumulated result of a simple equation applied relentlessly: a gap between income and spending, invested wisely, multiplied by time. Everything else — which fund to choose, how to allocate, when to rebalance — is detail layered on top of this foundation.

The Wealth Equation

Break the equation into its parts, and you can see exactly where wealth comes from — and where to focus.

The equation has four components, and improving any of them helps:

- Income — what you earn. Raising it (skills, career, side income) widens the potential gap.

- Spending — what you consume. Lowering it (consciously, not miserably) also widens the gap.

- The gap (savings rate) — the surplus between the two, the raw fuel of wealth.

- Time and compounding — the multiplier that turns the gap into wealth, as covered in Compound Growth.

Most people fixate on income alone, but income is only one of four levers — and as we'll see, often not the decisive one.

Why Savings Rate Beats Income

Here is the counter-intuitive truth at the heart of wealth-building: how much you keep usually matters more than how much you earn. Wealth comes from the gap, not the income, and a large income with an equally large spending habit produces a gap of zero — and therefore no wealth.

Consider two people. The first earns £100,000 but spends £98,000, saving £2,000 a year. The second earns £45,000 but spends £33,000, saving £12,000 a year. Despite earning less than half as much, the second person builds wealth six times faster — and invested over decades, that gap, compounded, becomes a vast difference in outcomes. We all know of high earners who are perpetually broke and modest earners who quietly become wealthy; the explanation is almost always the savings rate, not the salary. This is empowering, because while income can be hard to change quickly, your savings rate is largely within your control starting today. A higher income helps only if it widens the gap rather than the spending.

Your savings rate has another, deeper effect: it works on both sides of financial freedom at once. A higher savings rate means you both salt away more and learn to live on less — so the pot you need to become financially independent is smaller, and you reach it sooner. This double effect is why savings rate is so powerful.

The Enemy: Lifestyle Inflation

If savings rate is the key, its great enemy is lifestyle inflation — the natural tendency to spend more as you earn more. A pay rise feels like permission to upgrade the car, the home, the holidays; and so expenses creep up to swallow the extra income, leaving the savings gap no bigger than before. This is why so many people earn dramatically more over their careers yet never build proportionate wealth: every raise was absorbed by lifestyle rather than directed to the gap.

The antidote is not deprivation but intention: when income rises, deliberately direct a meaningful share of the increase to investing before lifestyle expands to claim it. Even keeping spending flat through one or two raises, and banking the difference, can transform your trajectory. Enjoying some of your success is reasonable and human — the point is to do it consciously, keeping the gap growing rather than letting it quietly close. Controlling lifestyle inflation is often the single highest-impact financial habit a rising earner can build.

Widening The Gap From Both Ends

Since the gap is the fuel, it's worth knowing that you can widen it from two directions — and the most effective approach usually works both.

On the spending side, the biggest wins come from the largest, most recurring costs: housing, transport and food typically dominate a budget, so a sensible choice on where you live or what you drive moves the needle far more than cutting small daily treats. The aim is conscious spending — directing money toward what genuinely matters to you and trimming what doesn't — rather than joyless penny-pinching. Automating the gap (paying yourself first, as in Financial Goals) ensures the surplus is captured before it can be spent.

On the income side, raising your earning power — through skills, career progression, or additional income streams — can widen the gap without requiring you to cut anything, and unlike spending, income has no upper limit. The crucial discipline, as we've seen, is to channel income increases into the gap rather than letting lifestyle inflation absorb them. The most powerful wealth-builders typically attack both ends at once: steadily growing income while keeping spending growth slower, so the gap widens year after year. You don't have to choose between earning more and spending less — doing both, even modestly, compounds into a rapidly growing surplus to invest.

Put The Gap To Work

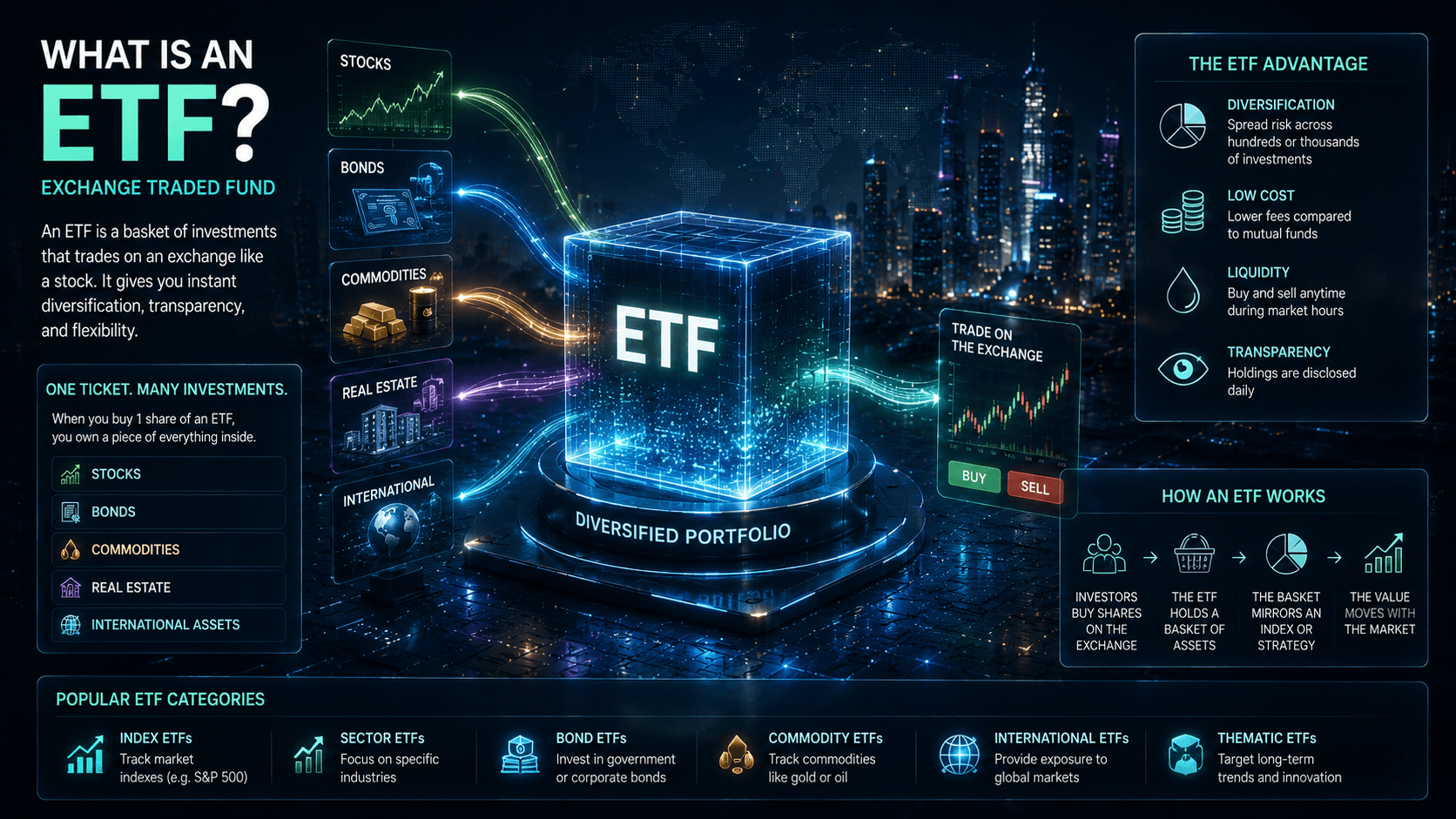

A savings gap sitting in cash is not yet wealth-building — inflation will erode it, as Inflation showed. The gap becomes wealth only when invested, so that compounding and the long-term growth of productive assets multiply it. For most people, this means a diversified, low-cost, long-term portfolio — exactly the approach the rest of the Ironclad curriculum builds toward, often anchored by broad funds (What Is An ETF?).

The mechanism is the compounding you've already met: the invested gap earns returns, those returns earn returns, and over decades the total dwarfs the contributions. This is why the two halves — saving the gap and investing it — must work together. Saving without investing loses to inflation; "investing" without a savings gap to invest has nothing to work with. Wealth lives at the intersection: a consistent gap, consistently invested, consistently compounding.

Consistency Beats Brilliance

Perhaps the most reassuring lesson in all of wealth-building is that you do not need to be brilliant. You do not need to pick the next great stock, time the market, or outsmart professionals. You need to be consistent — to invest regularly, automatically, for a very long time.

This flywheel is almost dull in its simplicity, and that's the point. The investor who automatically puts a fixed sum into a diversified fund every month for thirty years, ignoring the noise, will very likely outperform the clever one who jumps in and out trying to be smart — because consistency harnesses compounding while cleverness usually invites costs, taxes and mistakes. Automating the process (as in Financial Goals) removes willpower from the equation and lets the flywheel turn on its own. Wealth-building rewards the tortoise, not the hare.

Protect What You Build

Growing wealth is only half the job; the other half is protecting it, because a single catastrophe can undo years of patient progress, and losses are painfully asymmetric (a point from Risk vs Reward). Several safeguards matter:

- An emergency fund so a shock doesn't force you to sell investments or take on ruinous debt.

- Avoiding high-interest debt, which compounds against you as fiercely as investments compound for you.

- Diversification, so no single failed company or bet can wipe out what you've built.

- Appropriate insurance for the genuinely catastrophic risks (health, income, home), which protects your wealth from being consumed by disaster.

- Avoiding ruin — never taking a risk, however tempting, that could permanently destroy a large part of your wealth.

The mindset shift is to value not losing as highly as gaining. A spectacular year means little if a later disaster erases it; steady building protected against catastrophe is what actually compounds into lasting wealth. (The full treatment lives in What Is Risk Management?.)

What Wealth Is Actually For

It's worth stepping back to ask what all this building is for, because wealth is a means, not an end. Beyond a basic level of security, money's greatest value is not the things it buys but the freedom and options it provides: the freedom to weather a job loss without panic, to leave a bad situation, to take a career risk, to retire with dignity, to help the people you love, to spend your time more on your own terms. Wealth, used well, is stored choice.

Keeping this in view matters for two reasons. First, it sustains motivation through the long, sometimes dull middle of the journey — saving is easier when you remember it's buying freedom, not just a bigger number. Second, it guards against the trap of accumulating for its own sake while never actually living: the goal is a life well lived, supported by financial security, not a spreadsheet maximised at the expense of everything else. Build wealth deliberately and patiently — but remember it's in service of the life you want, which is exactly why setting clear financial goals (the previous lesson) matters so much. Wealth without purpose is just a number; wealth aligned to your goals is freedom.

Common Misconceptions

- "You need a high income to build wealth." Helpful, but not decisive — savings rate and consistency matter more, and many high earners build little.

- "Wealth comes from finding the right investment." It comes overwhelmingly from the savings gap, invested steadily and compounded; investment selection is secondary.

- "I'll start building wealth once I earn more." Lifestyle inflation usually absorbs the extra; starting now, at any income, with whatever gap you can manage, beats waiting.

- "It has to be complicated." The core is a one-sentence equation; complexity is mostly optional detail, and simplicity is a feature, not a compromise.

Real-World Application

Picture an ordinary person on an average income who decides, at 30, to live a little below their means — saving 15% of what they earn — and to invest it automatically each month in a low-cost diversified fund, leaving it alone. They never earn a fortune, never pick a winning stock, never time the market. They simply keep the flywheel turning: earn, save the gap, invest, compound, repeat. They guard against disaster with an emergency fund and insurance, and they resist upgrading their lifestyle with every raise. Three decades later, that unremarkable, almost boring discipline has very likely made them genuinely wealthy — not through any single brilliant decision, but through the relentless application of a simple equation over time. This is how wealth is actually built. It is available to almost anyone willing to be patient, and it is the destination the entire Getting Started curriculum has been guiding you toward.

Key Takeaways

- Building wealth = spend less than you earn, invest the gap, and let it compound — repeated consistently over time.

- The savings rate (the gap) usually matters more than income; a modest earner who saves can out-build a high earner who spends.

- Lifestyle inflation is the main enemy — direct rises to the gap before spending claims them.

- The gap becomes wealth only when invested, so compounding and asset growth can multiply it; cash alone is eroded by inflation.

- Consistency beats brilliance — automate regular, long-term investing and let the flywheel turn; you needn't pick winners or time markets.

- Protect what you build — emergency fund, no ruinous debt, diversification, insurance, and avoiding catastrophic risk — because losses are hard to recover.

Finished this lesson? Track your progress.

Next lesson

Continue learning

What Is A Stock?

Related topics

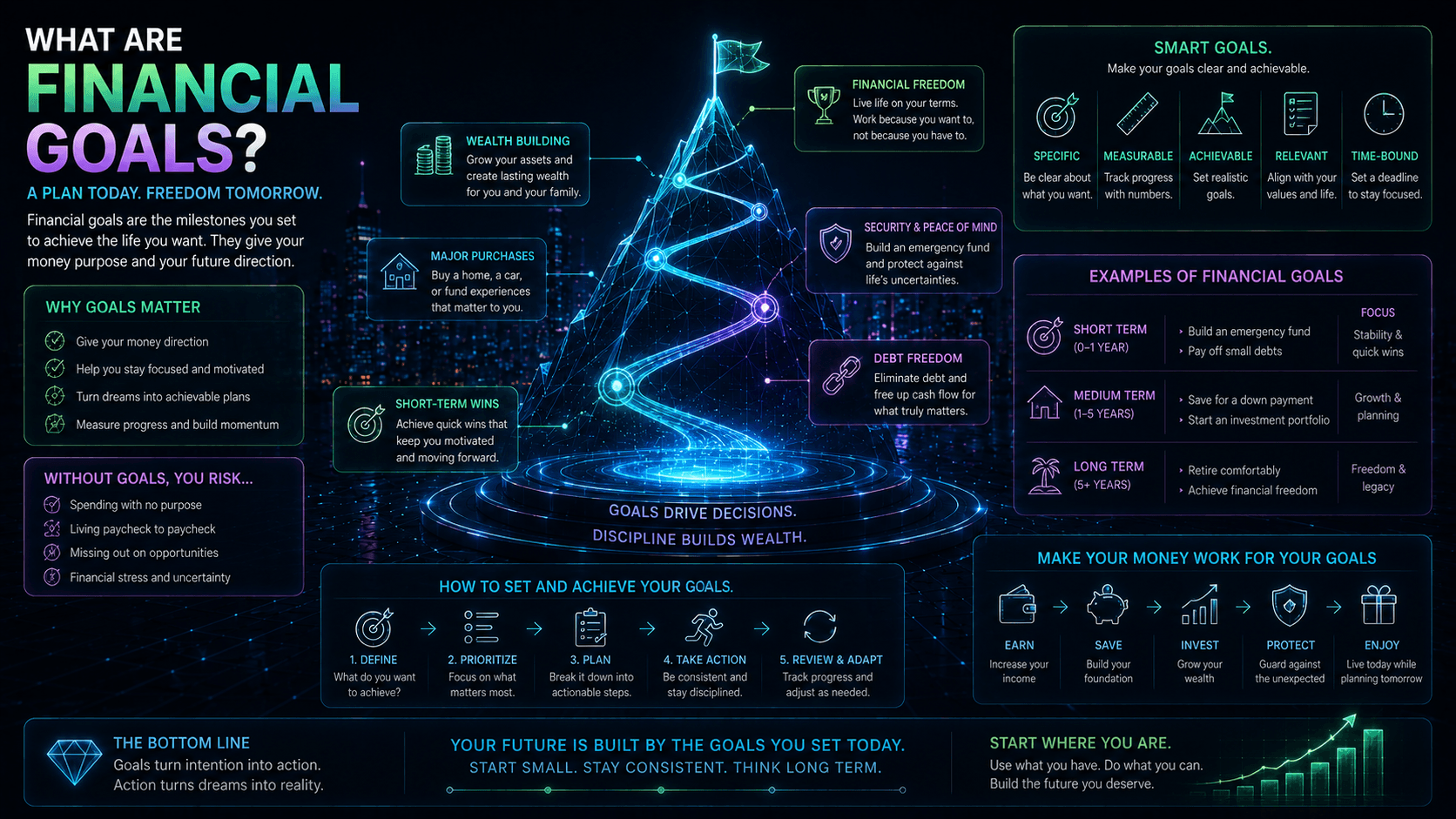

Financial Goals

Why clear goals are the starting point of all investing: how to set them, sort them by time horizon, match each to the right risk and account, and prioritise them through a sensible financial order of operations.

What Is An ETF?

A complete guide to exchange-traded funds: what they are, how they deliver instant diversification, how they track an index, why low costs matter so much, the main types, and the risks.

Ironclad Research provides educational content only. Nothing on this platform is financial advice, a recommendation, or an offer to buy or sell any security. Always do your own research and consider professional advice before making financial decisions.