Risk vs Reward

The single most important relationship in finance: why higher potential reward almost always comes with higher risk, how each is measured, the asymmetry of losses, and how to think about the trade-off sensibly.

Before this, read

Introduction

If you learn only one principle in all of finance, make it this one: reward and risk are joined at the hip. The chance to earn more almost always comes bundled with a greater chance of losing — and anyone who promises high returns with no real risk is either mistaken or trying to deceive you. This single relationship underpins every investment decision you will ever make, from choosing between a savings account and the stock market to deciding how much of your money to put at stake.

This lesson explains why the trade-off exists, how reward and risk are each measured, why losses hurt more than equivalent gains help, and — most importantly — how to think about the trade-off intelligently rather than being seduced by reward or paralysed by risk. It builds directly on What Is Investing? and lays the groundwork for the full treatment in What Is Risk Management?.

Quick Definition

The risk-reward trade-off is the principle that higher potential returns can only be pursued by accepting higher risk — the possibility of larger, and sometimes permanent, losses.

"Risk" here means uncertainty of outcome, including the chance of loss. "Reward" means the return you might earn. The trade-off says these two move together: you cannot reliably increase one without increasing the other. The whole craft of investing is not about escaping this trade-off — that is impossible — but about taking an appropriate amount of risk for the reward you seek, and being properly compensated for it.

Why The Trade-Off Exists

Why can't you have high reward at low risk? The answer comes from how markets price things. Imagine two assets offering the same expected return, but one is far riskier than the other. Every rational investor would prefer the safer one — so they would buy it, pushing its price up and its future return down, while selling the risky one, pushing its price down and its future return up. This continues until the risky asset offers a higher expected return to compensate for its risk. Otherwise, no one would hold it.

This is the risk premium: the extra expected return that risky assets must offer to persuade investors to bear their risk. It is why shares have historically returned more than bonds, and bonds more than cash — each step up the risk ladder demands a reward to match. The trade-off is not a rule imposed by anyone; it emerges naturally from millions of investors weighing risk against reward and pricing assets accordingly. The crucial word, though, is expected: the higher return is a probability, not a promise. Taking more risk gives you a shot at more reward — and also a real chance of the loss that is the very reason the reward was on offer.

The Risk-Reward Spectrum

Different assets sit at different points on the trade-off, forming a spectrum from safe-but-low-return to risky-but-potentially-high-return.

Cash is the safest in nominal terms but barely grows and loses real value to inflation. Bonds offer modest, steadier returns. Diversified funds of shares offer higher expected returns with significant but manageable volatility. Individual shares raise both the potential reward and the risk of a single company faltering. Speculative assets — highly volatile instruments, leverage, or unproven ventures — dangle the largest potential returns alongside the largest chance of severe loss. Crucially, no point on this line is "best": the right place for your money depends on your goals, your time horizon and your tolerance for the ride.

Measuring Reward And Risk

To think clearly about the trade-off, you need to measure both sides.

Reward is straightforward: it is the return, the percentage gain (or loss) on your money over a period, ideally measured after costs, taxes and inflation. What matters is the real, net return you actually keep.

Risk is subtler, because it has several faces. The two most common measures are:

- Volatility — how much an asset's returns fluctuate around their average. A highly volatile asset swings widely up and down; a low-volatility one moves gently. Greater volatility means more uncertainty about where you will end up at any given moment.

- Drawdown — the decline from a peak value to a subsequent low. Where volatility describes the general bumpiness, drawdown captures the worst of the pain: a portfolio that falls 40% from its high has suffered a 40% drawdown, and recovering from it is hard both mathematically and emotionally.

Other dimensions of risk matter too — the danger of permanent loss, of needing your money at a bad moment, of inflation eroding "safe" cash — but volatility and drawdown are the everyday language of measuring how risky an investment is.

Risk is not one thing

It helps to recognise that "risk" is really a family of distinct dangers, and the trade-off applies to each:

- Market risk — the whole market can fall, dragging even good, diversified holdings down. This is the volatility most people picture, and it cannot be diversified away within an asset class.

- Specific (concentration) risk — the danger that one company, sector or country you're over-exposed to fails. Unlike market risk, this one can be reduced through diversification.

- Inflation risk — the quiet erosion of purchasing power, the danger that your money grows slower than prices rise. It is the risk that "safe" cash is most exposed to.

- Liquidity risk — the danger of not being able to sell when you need to, at a fair price, common in obscure or thinly traded assets.

- Permanent-loss risk — the difference between a temporary fall you recover from and money you never get back, often the result of excessive concentration or leverage.

A sophisticated view of the trade-off weighs all of these, not just price volatility. Reducing one kind of risk frequently increases another — flee market risk into cash and inflation risk rises; chase high returns and concentration and permanent-loss risk grow. There is no risk-free corner of the map; there is only a thoughtful balance.

The Asymmetry Of Loss

A vital and counter-intuitive feature of the trade-off is that losses and gains are not symmetrical — losses hurt more than equivalent gains help, because after a loss you have less capital left to recover with.

A 10% loss needs only an 11% gain to recover — easy. But a 50% loss needs a 100% gain, and a 75% loss needs a 300% gain. As losses deepen, the climb back grows exponentially steeper, and at the extremes, recovery becomes practically impossible. This asymmetry transforms how you should weigh the trade-off: it means that avoiding catastrophic losses is more valuable than capturing the very highest returns. A strategy that earns slightly less but never suffers a devastating drawdown will often end up far ahead of a wilder one that periodically blows up. Reward is seductive; but it is the management of the downside that most often determines long-term success.

Risk-Adjusted Thinking

A natural beginner's instinct is to chase the highest possible return. The trade-off teaches a more sophisticated habit: judge investments by their risk-adjusted return — how much reward you earn per unit of risk taken — not by headline returns alone.

Consider two investments that both returned 10% last year. If the first did so with gentle, steady growth and the second with stomach-churning swings and a terrifying 50% drawdown along the way, they are not equally good, even though the headline number matches. The first delivered its reward far more efficiently and safely. An investment offering a 20% expected return with a real chance of total loss may be worse than one offering 8% with little chance of ruin, depending on your situation. Professionals formalise this with ratios that divide return by risk, but the core idea is simple and powerful: more reward is only better if the extra risk is worth it. Always ask not just "what could I earn?" but "what could I lose, and is the potential reward worth that risk?"

Diversification: A Rare Free Lunch

If the trade-off is iron, is there any way to get more reward for less risk? There is one, and it is sometimes called the only free lunch in finance: diversification.

Because different assets do not all move together, combining them causes their individual ups and downs to partly cancel out. The result is a portfolio whose overall volatility is lower than the average of its parts, often without sacrificing expected return. In effect, diversification lets you move up and to the left on the risk-reward chart — more reward per unit of risk — which is why it is so prized. It does not abolish the trade-off (a diversified portfolio still carries market risk and still falls in a broad downturn), but it genuinely improves the terms, and it is available to everyone through low-cost funds. It is the closest thing investing offers to getting something for nothing.

How Time Horizon Changes The Trade-Off

The trade-off is not fixed — it bends with your time horizon. Over a single day or year, a volatile asset like shares is genuinely risky: it could easily fall sharply, and if you needed the money then, you would be forced to sell at a loss. But over decades, that same asset's higher expected return becomes far more reliably accessible, because downturns have time to recover and compounding has time to work.

This means the right amount of risk depends on when you will need the money. Money required next year should sit at the low-risk end of the spectrum, where a sudden drawdown can't hurt you. Money you won't touch for thirty years can sensibly accept far more risk, because the long horizon tames the volatility and lets the risk premium pay off. Time, in other words, is a tool for converting risk into reward — one of the most powerful an investor has.

Matching Risk To Yourself

Putting it together, the practical question is not "how do I avoid risk?" or "how do I maximise reward?" but "how much risk is right for me?" The answer depends on three things: your goals (what the money is for), your time horizon (when you need it), and your temperament (how much volatility you can endure without panic-selling). An aggressive portfolio is worthless if its drawdowns frighten you into abandoning it at the bottom; a too-cautious one may fail to grow enough to meet your goals, with inflation quietly eroding it. The sweet spot is the most risk you can take that still lets you sleep at night and stay the course — enough to be rewarded, not so much that you self-destruct.

The Risk Of Playing It Too Safe

The trade-off is usually taught as a warning against taking too much risk — and that warning is important. But there is an equal and opposite danger that beginners often overlook: taking too little. Holding all your money in cash feels safe because the number never drops, yet over long periods it is one of the riskiest things you can do with money meant to grow, because inflation steadily erodes what it can buy.

Consider someone who keeps their entire retirement savings in cash for thirty years to "avoid risk." They avoid market volatility entirely — and in doing so, they almost guarantee a different, quieter loss: their money's purchasing power shrinks year after year, and they forgo three decades of the risk premium that would have grown it many times over. The "safe" choice may leave them unable to meet their goals — a far worse outcome than enduring some volatility along the way. This is the paradox at the heart of the trade-off: refusing to take any risk is itself a risk, often a serious one for long-term money. The goal is never to minimise risk to zero, but to take the right risk for your horizon and goals — enough that your money can grow, matched to a level you can endure.

Common Misconceptions

- "Some investments offer high returns with no risk." Treat this claim as a red flag for a scam or a misunderstanding; the risk is always there, even if hidden.

- "Low risk is always safer." Holding only cash feels safe but carries inflation risk — the near-certain erosion of purchasing power over time. Avoiding all market risk is itself a risky choice.

- "The highest-returning investment is the best." Only on a risk-adjusted basis, and only if the risk suits your situation; headline returns alone are misleading.

- "Diversification limits my gains." It moderates the extremes, but it improves reward per unit of risk and protects against ruin — a trade most long-term investors should happily make.

Real-World Application

Suppose you have £10,000 and two timelines: £2,000 you'll need for a holiday next year, and £8,000 for retirement in thirty years. The risk-reward principle gives a clear, differentiated answer. The £2,000 belongs at the low-risk end — cash or a savings account — because a market drop next year could force a loss you can't recover in time; the modest return is the price of safety you genuinely need. The £8,000, by contrast, can sit in a diversified, higher-risk portfolio of shares, because three decades give the risk premium time to pay and downturns time to heal. Same person, same total money, two completely different risk choices — each correctly matched to its purpose. That is the risk-reward trade-off working for you: not avoided, but deliberately and intelligently chosen.

Key Takeaways

- Higher potential reward almost always means higher risk — there is no reliable free lunch of big returns at low risk.

- The risk premium explains why shares out-return bonds and bonds out-return cash; the extra return is expected, never guaranteed.

- Reward is measured by return; risk by volatility and drawdown — and losses are asymmetric, so avoiding deep losses matters more than chasing the highest gains.

- Judge investments by risk-adjusted return, not headline numbers; diversification improves the trade-off, the closest thing to a free lunch.

- A longer time horizon converts risk into reward; match your risk to your goals, horizon and temperament.

Finished this lesson? Track your progress.

Next lesson

Continue learning

Inflation

Related topics

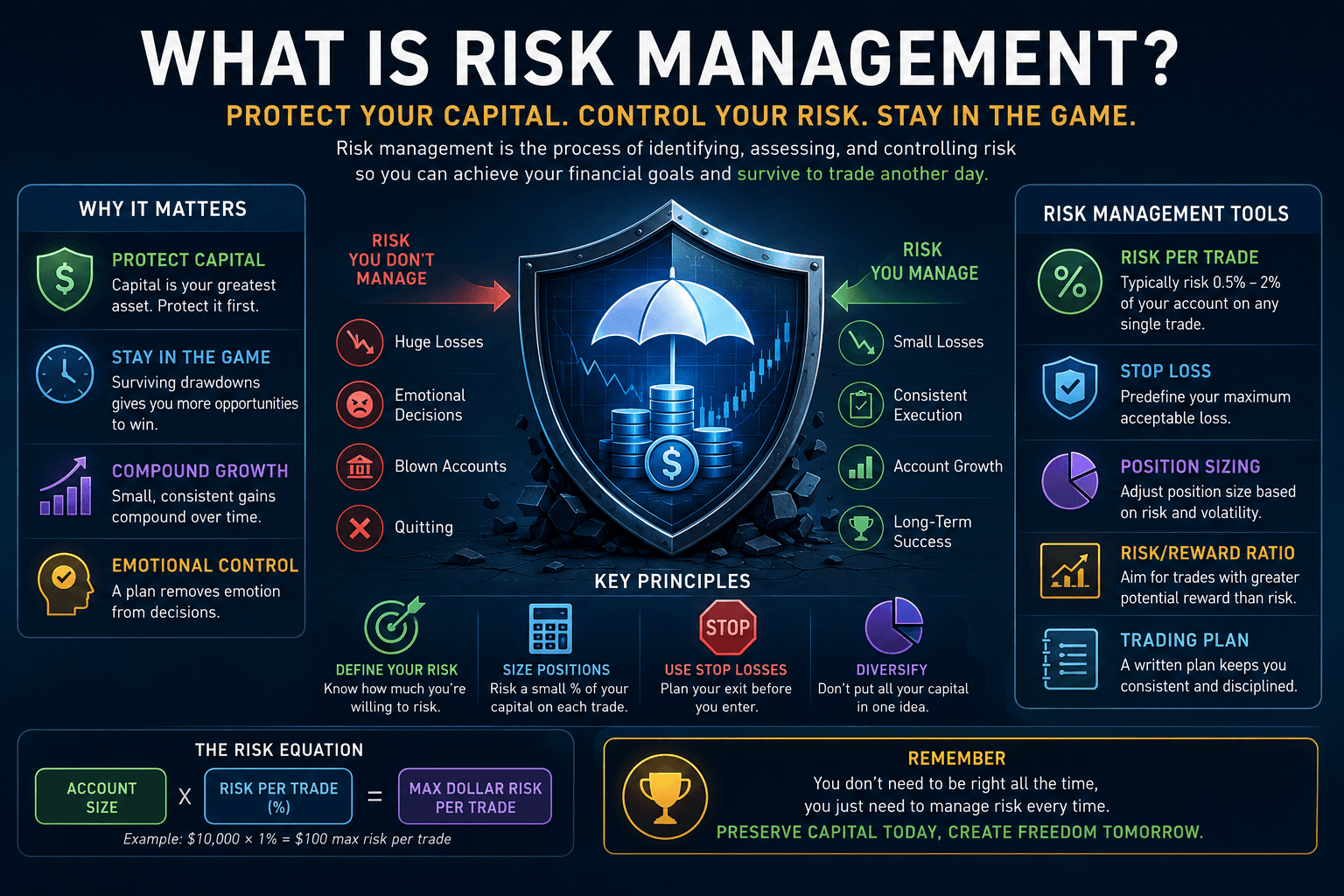

What Is Risk Management?

A practical guide to the discipline that protects investors: why avoiding ruin matters more than maximising gains, the brutal maths of large losses, position sizing, diversification, drawdowns, and matching risk to your goals.

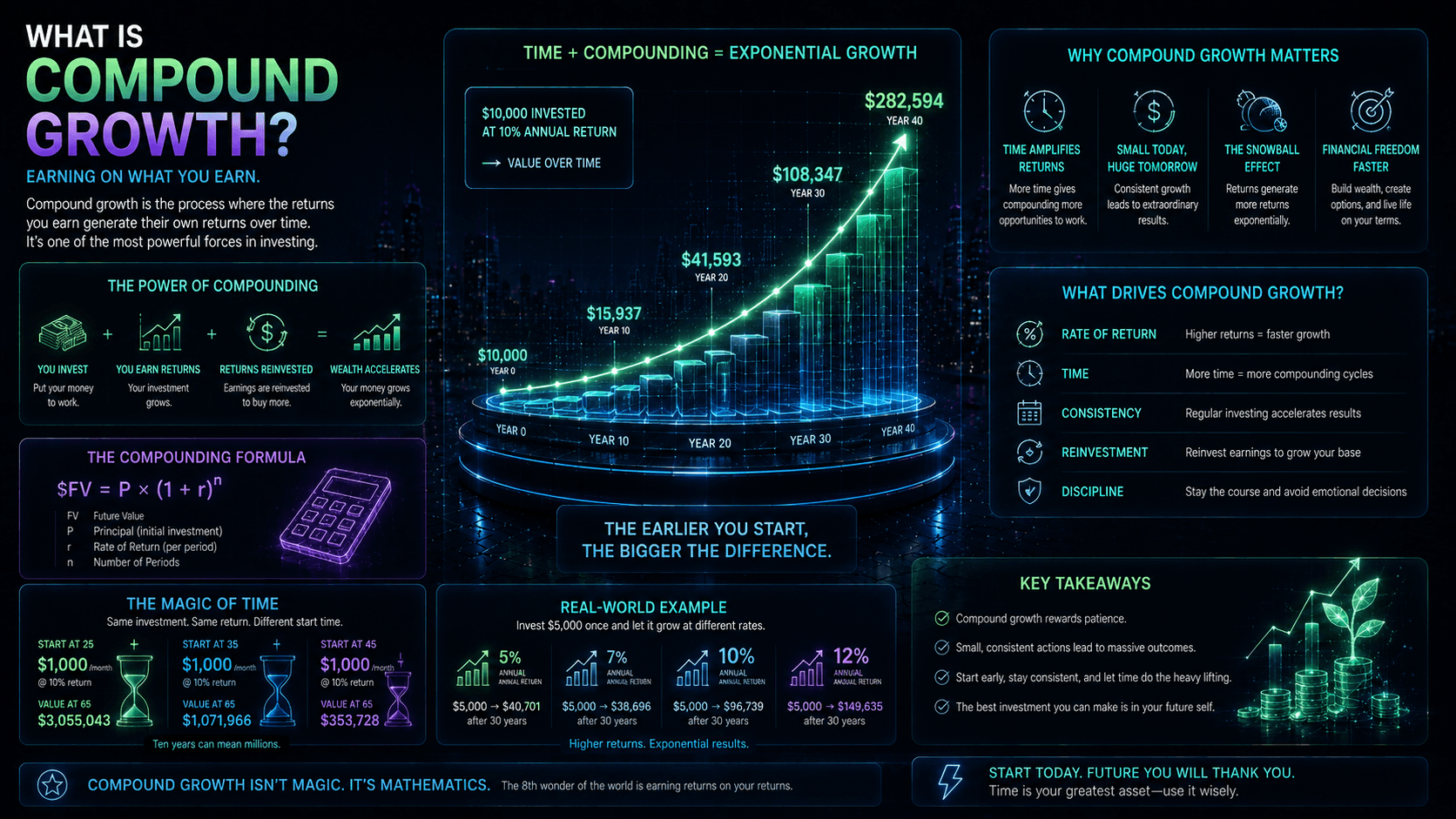

Compound Growth

The most powerful force in investing: how returns earning returns turns modest sums into large ones over time, the three levers that drive it, why starting early matters most, and how compounding can work against you too.

Ironclad Research provides educational content only. Nothing on this platform is financial advice, a recommendation, or an offer to buy or sell any security. Always do your own research and consider professional advice before making financial decisions.