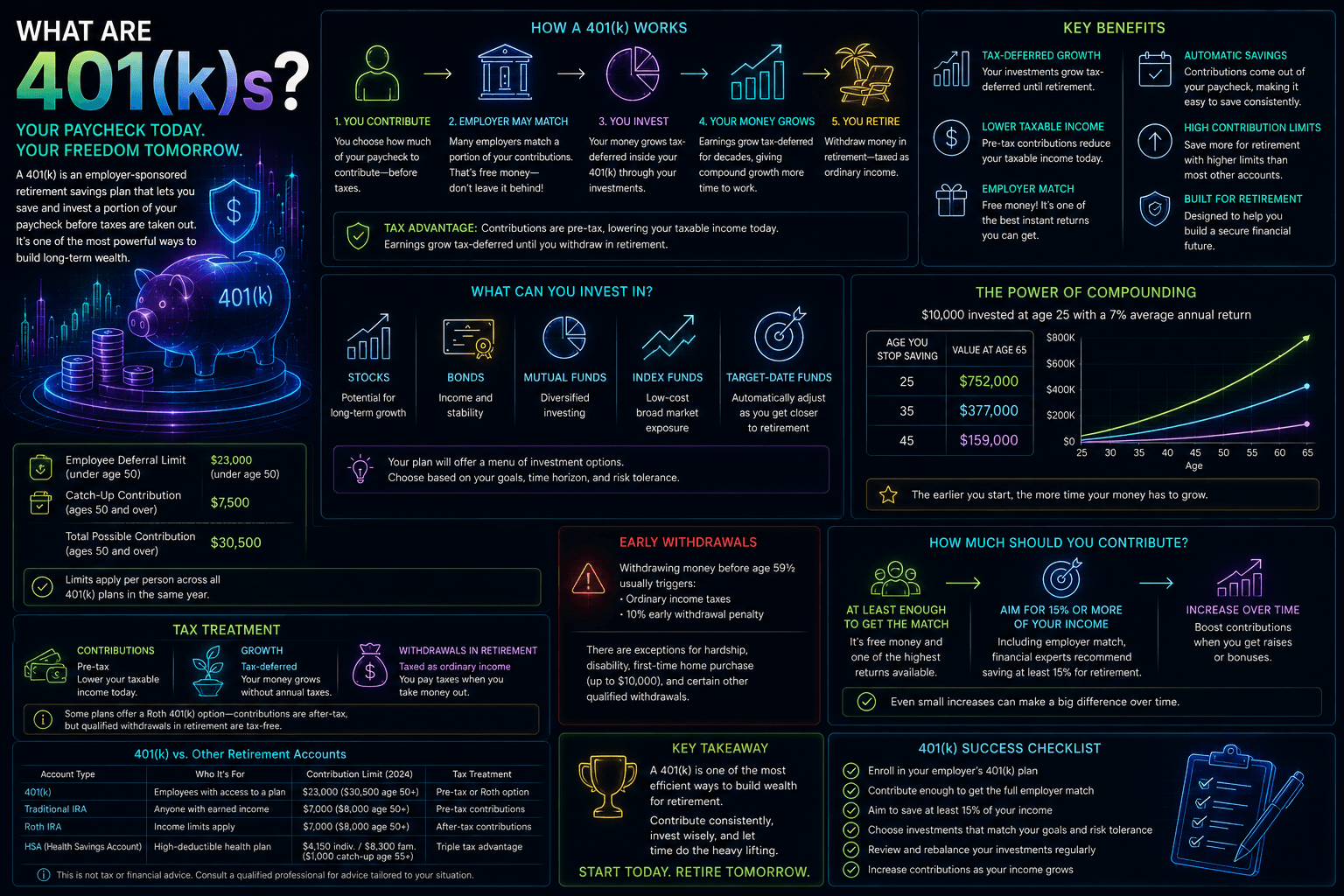

Traditional IRA

The individual US retirement account you open yourself: how Traditional IRA contributions can be tax-deductible, how tax-deferred growth compounds, how it differs from a 401(k), the annual limit, and the rules on deductibility, early access and required withdrawals.

Before this, read

Introduction

A 401(k) is powerful, but it has two limits: you only get one through an employer, and you're confined to the plan's menu of funds. The Traditional IRA fills both gaps. It's a retirement account you open yourself, directly with a broker, giving you a wide universe of investments and a valuable slice of tax-advantaged space — whether or not you have a workplace plan.

This lesson explains what a Traditional IRA is, how its contributions can be tax-deductible, how tax-deferred growth compounds, how it compares with a 401(k), and the key rules around limits, deductibility, early access and required withdrawals. (Tax rules are US-specific and can change; this is education, not tax advice.)

Quick Definition

A Traditional IRA is an individual US retirement account you open yourself. Contributions may be tax-deductible, the money grows tax-deferred, and you pay ordinary income tax when you withdraw in retirement.

"IRA" stands for Individual Retirement Arrangement (commonly, "account"). The word individual is the key contrast with a 401(k): there's no employer involved. You set it up, you fund it, and you choose what it holds.

How A Traditional IRA Works

You open a Traditional IRA at a broker (comparing them on cost and features, as in Choosing A Broker), contribute money up to the annual limit, and invest it in almost anything the broker offers — individual stocks, bonds, and especially low-cost, diversified funds (see What Is An ETF?). From then on, everything inside the account grows tax-deferred: no tax on dividends, interest, or capital gains as it compounds, year after year.

The tax treatment has two stages:

- Going in — contributions may be tax-deductible, reducing your taxable income for the year. Whether (and how much) you can deduct depends on your income and whether you or a spouse are covered by a workplace plan like a 401(k).

- Coming out — withdrawals in retirement are taxed as ordinary income. You deferred the tax; now it comes due.

This "deduct now, tax later" shape is the same trade as a pre-tax 401(k) — the difference is simply that you, not an employer, own and direct the account.

Traditional IRA vs 401(k)

The IRA and the 401(k) are complementary, not competing. Understanding how they differ tells you when to use each.

The most important practical point: because an IRA has no employer match, it usually comes after claiming the full 401(k) match in the priority order (see 401(k)). But the IRA's far wider investment menu and extra tax-advantaged space make it a natural next step once the match is secured.

Contribution Limits And Deductibility

Two rules shape how much benefit you get:

- The annual limit. The IRS caps how much you can contribute to all your IRAs combined each year, with an extra catch-up amount for those age 50 and older. The IRA limit is considerably smaller than the 401(k) limit, and the figures change over time — check the current year rather than relying on an old number.

- Deductibility. You can always contribute (if you have earned income), but whether the contribution is tax-deductible can be reduced or eliminated at higher incomes if you or a spouse are covered by a workplace retirement plan. If your deduction is limited, a Roth IRA (see Roth IRA) is often the better individual account to consider.

This deductibility nuance is the main complication of the Traditional IRA, and it's exactly where the Roth IRA enters the picture as the alternative.

Accessing The Money

A Traditional IRA follows the same retirement-focused access rules as a pre-tax 401(k):

- Age 59½. Withdraw before then and you'll generally owe ordinary income tax plus a 10% early-withdrawal penalty, subject to specific exceptions (certain first-home purchases, qualified education or medical costs, disability, and others).

- Required Minimum Distributions (RMDs). Because the tax was deferred, the IRS eventually requires you to start withdrawing a minimum amount each year once you reach a set age — it wants its deferred tax in due course.

- Rollovers. When you leave a job, you can roll a 401(k) into a Traditional IRA, consolidating old workplace plans into one account with broader investment choice while preserving the tax treatment.

Risks & Considerations

- It shelters tax, not market risk. Investments inside still rise and fall; tax-deferral doesn't prevent losses.

- No match. Unlike a 401(k), there's no free employer money — which is why the match is usually claimed first.

- Deductibility can be limited. At higher incomes with a workplace plan, your deduction may shrink or vanish; know the rules before relying on the tax break.

- Early access is costly. The 10% penalty and taxes make pre-59½ withdrawals expensive.

- RMDs apply. Pre-tax money must eventually be drawn down and taxed; it can't grow tax-deferred forever.

Common Misconceptions

- "An IRA is provided by my employer." No — you open and fund an IRA yourself. The employer plan is the 401(k).

- "Contributions are always deductible." Deductibility can be limited at higher incomes if you're covered by a workplace plan.

- "An IRA and a 401(k) are the same thing." They're both tax-advantaged retirement accounts, but differ on who provides them, the match, investment choice and limits.

- "IRA money is tied to my job." It isn't — an IRA stays with you regardless of where (or whether) you work.

Real-World Application

Consider someone who already contributes enough to their 401(k) to capture the full employer match, and has more to save. They open a Traditional IRA at a low-cost broker and contribute up to the annual limit, investing in a broad index fund unavailable in their workplace plan. If eligible, they deduct the contribution, lowering this year's tax bill, and the balance compounds tax-deferred for decades. They've added tax-advantaged space and better investment choice on top of the workplace match — a textbook use of the two accounts together. They didn't chase returns; they used the structure the tax code provides.

Key Takeaways

- A Traditional IRA is an individual retirement account you open yourself at a broker — no employer involved.

- Contributions may be tax-deductible (subject to income and workplace-plan rules); growth is tax-deferred; withdrawals are taxed as income.

- Versus a 401(k): an IRA has no match and a smaller limit, but offers far more investment choice and flexibility.

- A common order is match first (401k), then IRA, then more 401(k) — the IRA's strength is choice and extra tax-advantaged room.

- The same access rules apply: age 59½, a 10% early-withdrawal penalty, and eventual RMDs.

- If your deduction is limited at higher income, a Roth IRA is often the better individual account to weigh next.

Finished this lesson? Track your progress.

Key terms

Next lesson

Continue learning

Roth IRA

Related topics

Ironclad Research provides educational content only. Nothing on this platform is financial advice, a recommendation, or an offer to buy or sell any security. Always do your own research and consider professional advice before making financial decisions.