Choosing A Broker

A practical framework for picking the right broker: why regulation and investor protection come first, how to judge true all-in cost, which account types and investments to check for, and how to match a broker to the way you actually invest.

Before this, read

Introduction

Choosing a broker is one of the first real decisions you'll make as an investor, and a foundational one — it's the firm that will hold your investments, execute your trades, and house your accounts, potentially for decades. Yet the choice is often made carelessly, swayed by a slick app or a "zero commission" banner. This lesson gives you a clear, practical framework to choose well, so you pick a broker that's safe, cheap for your style, and a good long-term home for your money.

Drawing together everything from the Brokers & Accounts category — what brokers do, how they make money, the costs you pay, and the accounts available — this is the decision-making capstone. It builds on What Is A Broker?, How Brokers Make Money and Commissions, and turns that knowledge into a checklist you can actually use.

Quick Definition

Choosing a broker means evaluating providers against what matters: regulation and protection (first and non-negotiable), true all-in cost, the account types and investments you need, execution quality, and reliability — then matching the best fit to how you invest.

There is no single "best broker" for everyone. The right choice depends on your circumstances — which is why a framework beats a recommendation. Learn what to weigh, and you can judge any broker, now and in the future.

First And Non-Negotiable: Regulation And Protection

Before comparing any features, one question outranks all others: is the broker properly regulated and protected? A regulated broker operates under a credible authority (such as the FCA in the UK), which imposes real safeguards: client assets kept separate from the firm's own, minimum capital requirements, rules on fair treatment and order execution, and membership of an investor-compensation scheme (like the FSCS) that protects clients up to a limit if the firm fails.

An unregulated "broker" — especially the unsolicited, too-good-to-be-true platforms that proliferate online — offers none of this. If it vanishes with your money, you may have no recourse at all. Checking regulation takes minutes: reputable regulators publish public registers of authorised firms, where you can confirm the broker is listed and that its details match exactly (beware "clone" scams that impersonate real firms). This check is the highest-value due diligence you can do, and no advertised feature, bonus or low price is ever worth bypassing it. A genuine investment that loses value is an acceptable risk; handing money to an unregulated platform is not investing at all.

The Decision Checklist

With regulation confirmed, weigh the legitimate options against the factors that matter:

- True all-in cost. As Commissions and How Brokers Make Money showed, the headline commission is only part of the story. Add spreads, currency-conversion fees, platform/account fees and any inactivity charges, estimated for your pattern of investing. A "free" broker can be dearer than one charging a small, transparent fee.

- Account types. For a UK investor, check the broker offers the tax-efficient wrappers you need — a Stocks & Shares ISA, and perhaps a SIPP (ISAs, SIPPs). Using these well can matter more than small differences in fees.

- Investments available. Make sure the broker offers what you intend to hold — broad low-cost funds, the shares or markets you want, in your preferred currencies.

- Execution quality. The prices you actually receive vary between brokers; over many trades this adds up. Harder to assess, but reputable brokers disclose execution data.

- Reliability and support. Does the platform stay up during volatile markets? Can you reach a human when something goes wrong? Boring until you need it, then vital.

Match The Broker To Yourself

The reason there's no universal "best broker" is that the criteria carry different weight for different investors. A buy-and-hold investor making occasional fund purchases inside an ISA cares most about low platform/holding fees, ISA/SIPP availability, and reliability — and barely about per-trade costs. A more active investor cares more about per-trade costs, execution quality and the range of markets. Someone holding foreign shares should weigh currency-conversion fees heavily, as these are often the largest cost. Someone wanting advice needs a different kind of broker entirely from a self-directed one.

So the right process is: list what you need (the accounts, investments, and trading pattern that fit your goals), then weigh brokers against those priorities — not against a generic "best buy" list. A broker that's perfect for a frequent trader may be poor value for a patient investor, and vice versa. Knowing yourself is half of choosing well.

In practice, a quick comparison process works well: shortlist two or three regulated brokers that offer the accounts and investments you need; for each, estimate the total annual cost for your realistic pattern (holding fees + your expected trades' costs + any FX); then break ties on reliability, usability and service. Ten minutes of this beats hours of reading reviews, because it grounds the choice in your actual numbers rather than someone else's.

Common Pitfalls

A few mistakes catch people repeatedly:

- Chasing "free." Choosing purely on zero commission while ignoring spreads, FX markups and platform fees — the classic error, since the "free" broker is sometimes the most expensive overall.

- Ignoring account types. Picking a broker that doesn't offer the ISA or SIPP you need, then paying unnecessary tax — often costlier than any fee difference.

- Overlooking FX fees. For investors in foreign shares, a high currency-conversion markup quietly dwarfs other costs.

- Being seduced by gamified apps. A design that encourages frequent trading (see How Brokers Make Money) can cost you far more in behaviour than you save in commission.

- Over-optimising. Endlessly hunting the theoretically cheapest broker can waste more time than it saves; once a broker is regulated, low-cost and fit for purpose, choosing it and getting invested matters more than shaving a basis point.

You Can Switch Later

A reassuring point: choosing a broker is important, but it is not an irreversible, life-long commitment. If your needs change or a better option appears, you can usually transfer your investments to another broker — often "in-specie" (moving the holdings themselves, without selling), which avoids realising gains and staying out of the market. Transfers take some time and paperwork, and occasionally exit fees apply, so it's worth choosing well first. But the knowledge that you're not locked in should ease the pressure: make a sound, well-researched choice now, and adjust later if you need to. Don't let fear of a "wrong" choice keep you from starting at all.

Risks & Considerations

- Unregulated platforms are the biggest danger — always verify regulation and protection first.

- Hidden costs distort comparisons — judge total cost, not headlines.

- The cheapest broker isn't always best — protection, account types and reliability matter too.

- Switching has friction — possible but not instant, so choose thoughtfully.

- Your needs evolve — the right broker today may not be the right one in ten years; reassess occasionally.

Common Misconceptions

- "The best broker is whichever is cheapest / free." Best means safe, fit-for-purpose and low all-in cost for you — not just a low headline.

- "All regulated brokers are basically identical." They differ on cost, accounts, investments, execution and reliability.

- "Choosing a broker locks me in forever." You can transfer to another broker later.

- "A nice app means a good broker." Polish is not protection, low cost, or good execution — look past the interface.

Real-World Application

Imagine a new UK investor comparing two brokers. Broker A is a flashy, "commission-free" app with a gamified interface; Broker B is a plainer platform charging a small, capped annual fee. The naive choice is A on price. But applying the framework: both are regulated (good). On all-in cost, A earns through wide FX margins and keeps the interest on cash, while B is transparent and offers a Stocks & Shares ISA with low holding fees — and our investor wants to hold global funds in an ISA for the long term. For their needs, Broker B is cheaper, better-aligned, and a sounder long-term home, despite the visible fee. By choosing on regulation, true cost, account fit and their own style — not the "free" headline — they make a genuinely better decision. That is the whole point of a framework: it turns a marketing-driven guess into a reasoned choice.

Key Takeaways

- Regulation and investor protection come first — verify them before anything else; no feature justifies skipping this.

- Judge true all-in cost for your style — commissions, spreads, FX, platform and account fees — not the headline.

- Check the account types (ISA, SIPP) and investments you need; the right wrapper can matter more than small fee differences.

- Weigh execution quality and reliability, and match the broker to how you actually invest — there's no universal best.

- Avoid pitfalls: chasing "free," ignoring FX, and gamified overtrading.

- You can switch later, so choose thoughtfully but don't let perfectionism stop you starting.

Finished this lesson? Track your progress.

Key terms

Next lesson

Continue learning

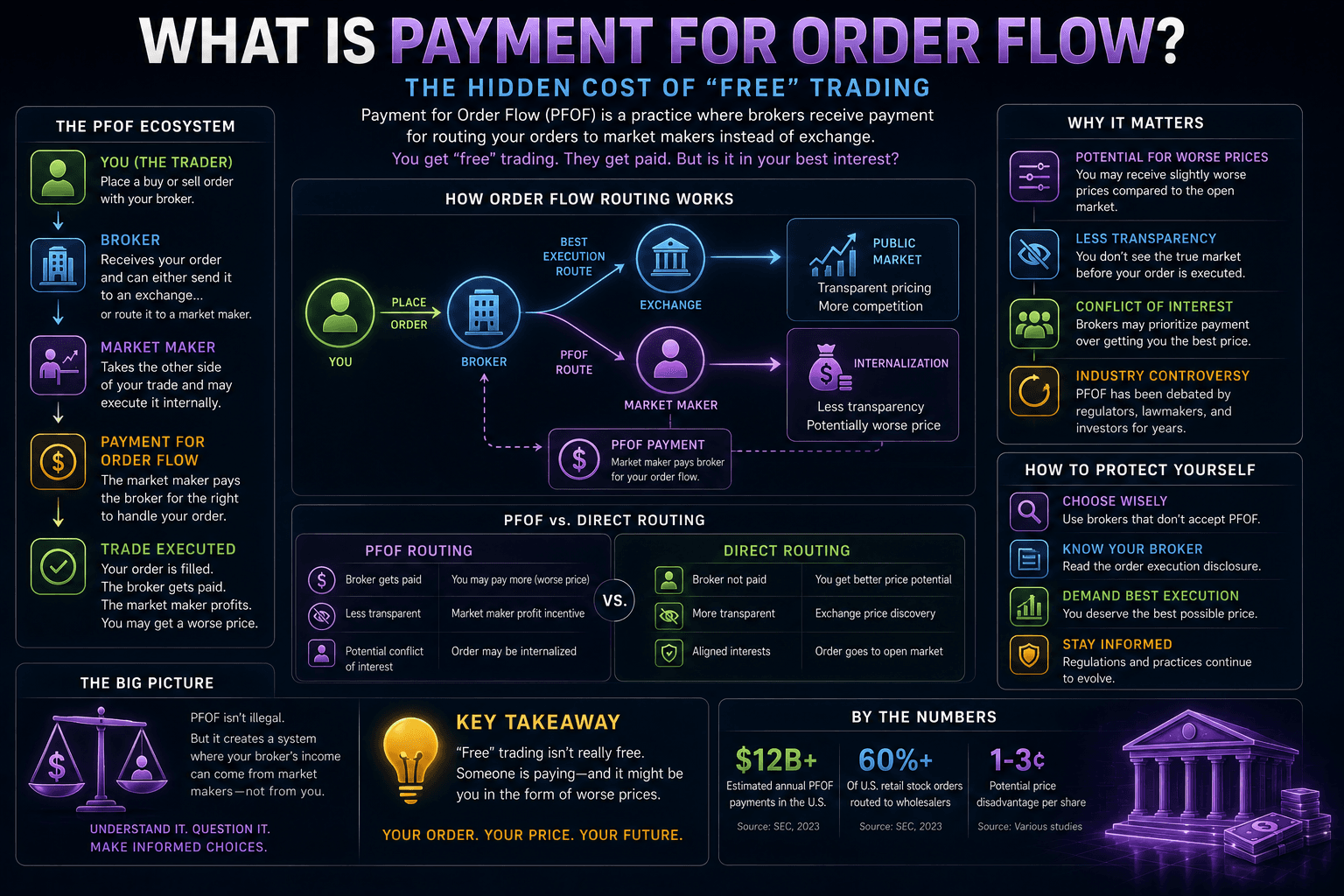

How Brokers Make Money

Related topics

Ironclad Research provides educational content only. Nothing on this platform is financial advice, a recommendation, or an offer to buy or sell any security. Always do your own research and consider professional advice before making financial decisions.