GC: Gold Futures

Gold (GC) is the benchmark precious-metals future — the market's classic safe haven and store of value. Learn its specifications, what actually drives the gold price (real interest rates, the dollar, fear and inflation expectations), why gold pays no yield, and how it's used as a portfolio diversifier.

Written by James Lipyeat · Founder, Ironclad Research

Reviewed 17 July 2026 · Editorial policy

Before this, read

Introduction

For thousands of years, across every civilisation, gold has meant wealth. In modern markets, that ancient role lives on through GC — the benchmark gold futures contract. Gold is the market's classic safe haven: the asset investors flee to when confidence in everything else — governments, currencies, banks, stock markets — wavers. GC is where the global gold price is discovered and hedged around the clock.

Gold is a strange asset. It pays no interest, produces nothing, and has few industrial uses relative to its price. Its entire value rests on a shared, enduring belief that it is a store of value. Understanding what actually moves it — and why it behaves so differently from shares — is what this final article in the Futures category is about.

Quick Definition

GC is the futures contract on gold, representing 100 troy ounces per contract. It's the primary market for trading and hedging the gold price, prized as a safe-haven asset and a hedge against uncertainty.

Key Specifications

- Underlying: physical gold

- Contract size: 100 troy ounces

- Tick size / value: $0.10 per ounce = $10.00 per contract

- Settlement: physical delivery

- Expiries: several months through the year

- Trading hours: nearly 24 hours a day, five days a week

- Smaller versions: the Micro (MGC) is 10 ounces (one-tenth), with other smaller contracts also available

With gold often trading well above $2,000 an ounce, one full GC contract can represent $200,000+ of gold — so the Micro (MGC) is the natural starting point for most individual traders.

What Actually Drives Gold

Gold confuses people because it doesn't respond to earnings or growth like a company does. Its price is driven by a distinct set of forces:

- Real interest rates. This is the big one. Because gold pays no yield, its main competitor is safe, interest-bearing assets like bonds. When real (inflation-adjusted) rates rise, holding zero-yield gold costs you the interest you're giving up — the opportunity cost rises — and gold tends to fall. When real rates fall, gold tends to shine. (This ties directly to Interest Rates.)

- The US dollar. Gold is priced in dollars, so a stronger dollar makes it more expensive for buyers in other currencies, usually weighing on the price; a weaker dollar tends to support it.

- Fear and uncertainty. In crises, wars and financial panics, safe-haven demand for gold can surge as investors seek something outside the financial system.

- Inflation expectations. Gold is often held as a hedge against inflation and currency debasement — the fear that paper money is losing value. The relationship is real over long horizons but looser and less reliable in the short term than many assume.

Why Gold Pays No Yield — And Why That Matters

Unlike shares (dividends) or bonds (coupons), gold produces no income. A bar of gold you hold for a decade is still just a bar of gold. This single fact shapes everything about how gold trades:

- Its appeal rises and falls with the opportunity cost of holding it — chiefly real interest rates.

- It is bought for price appreciation and protection, not income.

- It can languish for years when rates are high and confidence is strong, then rally hard when fear returns or rates fall.

Gold is, in essence, a bet on uncertainty and on the relative unattractiveness of everything that does pay a yield.

Gold's Role In A Portfolio

Despite its lack of income, gold earns a place in many portfolios as a diversifier and hedge. Because it often behaves differently from shares — sometimes rising sharply when markets fall — it can cushion a portfolio in exactly the crises that hurt everything else. It's also a hedge against loss of confidence in currencies and against extreme events. The trade-off is that it generates no income and can underperform for long stretches, so it's typically held as a modest, strategic slice rather than a core holding. Traders use GC (or the Micro MGC) both to speculate on these macro forces and to hedge other positions.

Common Misconceptions

"Gold always rises with inflation." Over the very long run gold has broadly preserved purchasing power, but the short-term link to inflation is loose. Gold has had long periods of falling prices even as costs rose — real interest rates and the dollar often matter more.

"Gold is risk-free." It's a safe haven, not a safe return. Gold is volatile and can fall substantially, and via GC it carries all the leverage risks of a future.

"Gold pays interest like a bond." It pays nothing. Its entire return is price change, which is why the opportunity cost of holding it — set by real rates — is so central.

"A strong economy is good for gold." Often the reverse — strong growth with rising real rates tends to dampen gold, while fear and falling rates tend to lift it.

Real-World Application

Imagine markets grow anxious: a geopolitical crisis erupts and investors fear a broad sell-off. Money flows into safe havens, and gold rises even as shares fall. A trader who anticipated this might be long GC (or the Micro MGC), profiting from the flight to safety while their equity positions suffer — gold acting as the portfolio hedge it's famous for.

Now consider the opposite regime: inflation is falling, the economy is strong, and the central bank keeps real interest rates high. Safe bonds now pay an attractive, real return, while gold still pays nothing. The opportunity cost of holding gold is high, and it drifts lower for months despite the occasional scare. A trader who understands that gold's great enemy is high real rates would size their exposure accordingly, rather than expecting it to rise simply because "gold is a store of value". That nuance — knowing gold responds to real rates, the dollar and fear rather than to growth or income — is what separates informed gold trading from folklore, and it's a fitting note to close the Futures category on.

Key Takeaways

- GC is the gold future — 100 troy ounces per contract, tick value $10, physically settled; the Micro (MGC) is 10 ounces.

- Gold is the classic safe haven and store of value, bought in fear and uncertainty.

- Its main driver is real interest rates (because gold pays no yield), alongside the US dollar, safe-haven demand and inflation expectations.

- Gold produces no income, so it's held for appreciation and protection, not yield — and can underperform for long stretches when real rates are high.

- In a portfolio it acts as a diversifier and hedge, typically a modest strategic allocation rather than a core holding.

Finished this lesson? Track your progress.

Key terms

Next lesson

Continue learning

ES: E-mini S&P 500 Futures

Related topics

CL: Crude Oil Futures

Crude oil (CL) is the world's most actively traded commodity future — a physically-settled contract on WTI crude, driven by geopolitics, OPEC and the global economy. Learn its specifications, why physical settlement matters, the meaning of contango and backwardation, and the cautionary tale of negative oil prices.

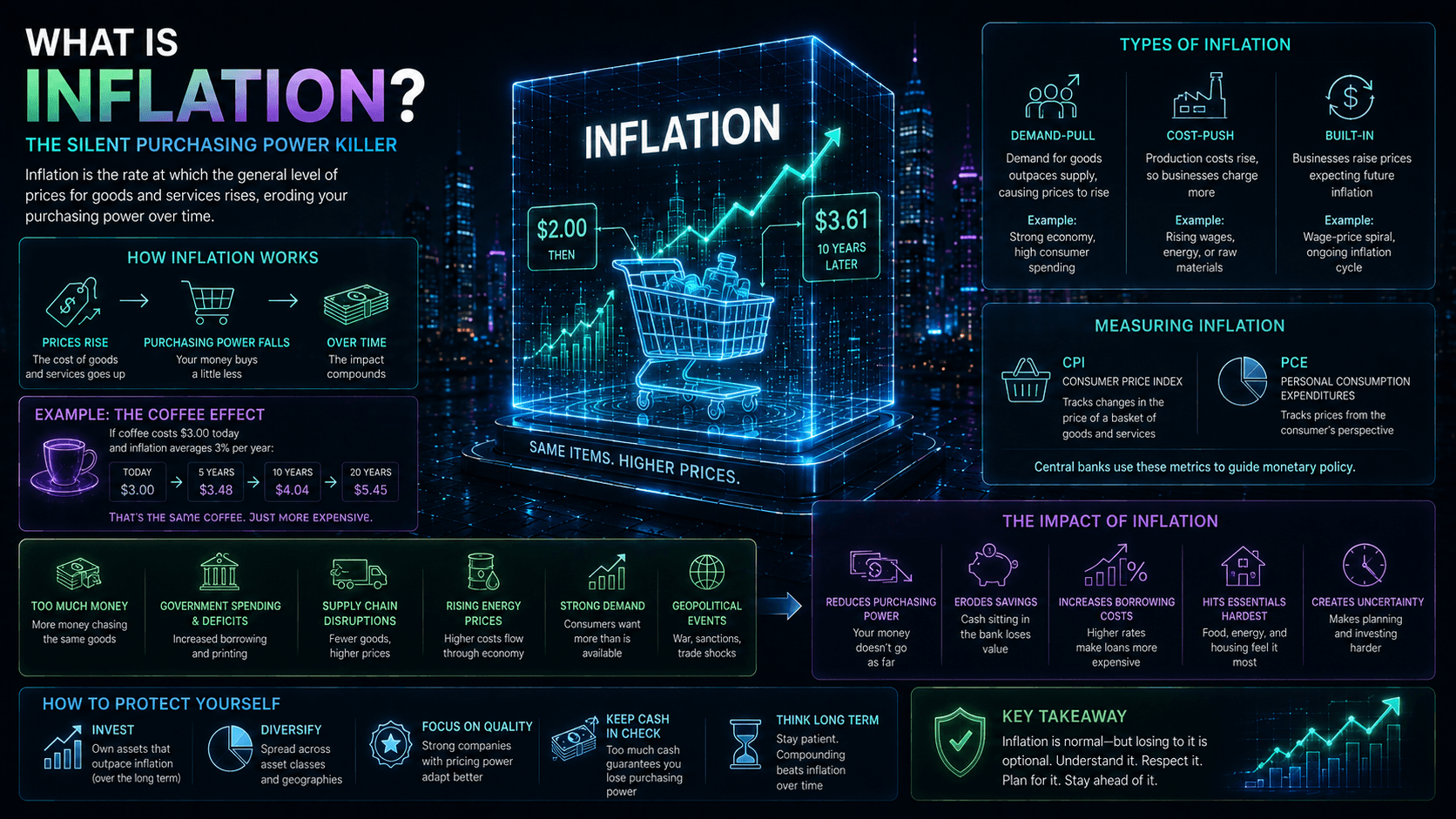

Inflation

Why the slow rise in prices is the quiet force every investor must beat: what inflation is, how it's measured, the difference between real and nominal returns, how it erodes idle cash, and how different assets hold up against it.

Futures Margin Requirements

Margin is the deposit that lets a small amount of capital control a large futures position — but it works nothing like stock margin. Learn the difference between initial and maintenance margin, how a margin call happens, why futures margin is a performance bond rather than a loan, and how to manage the leverage it creates.

Ironclad Research provides educational content only. Nothing on this platform is financial advice, a recommendation, or an offer to buy or sell any security. Always do your own research and consider professional advice before making financial decisions.